The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

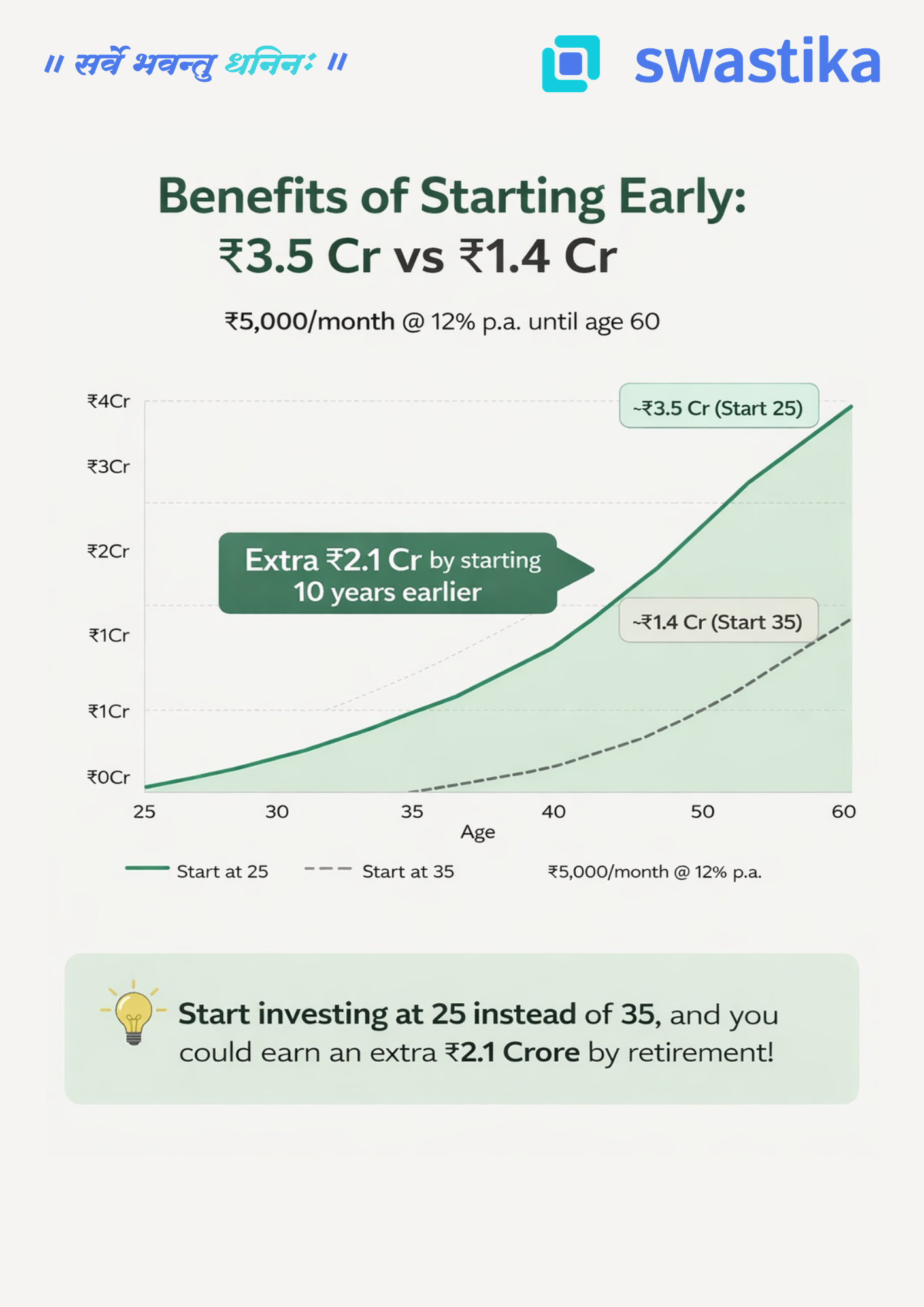

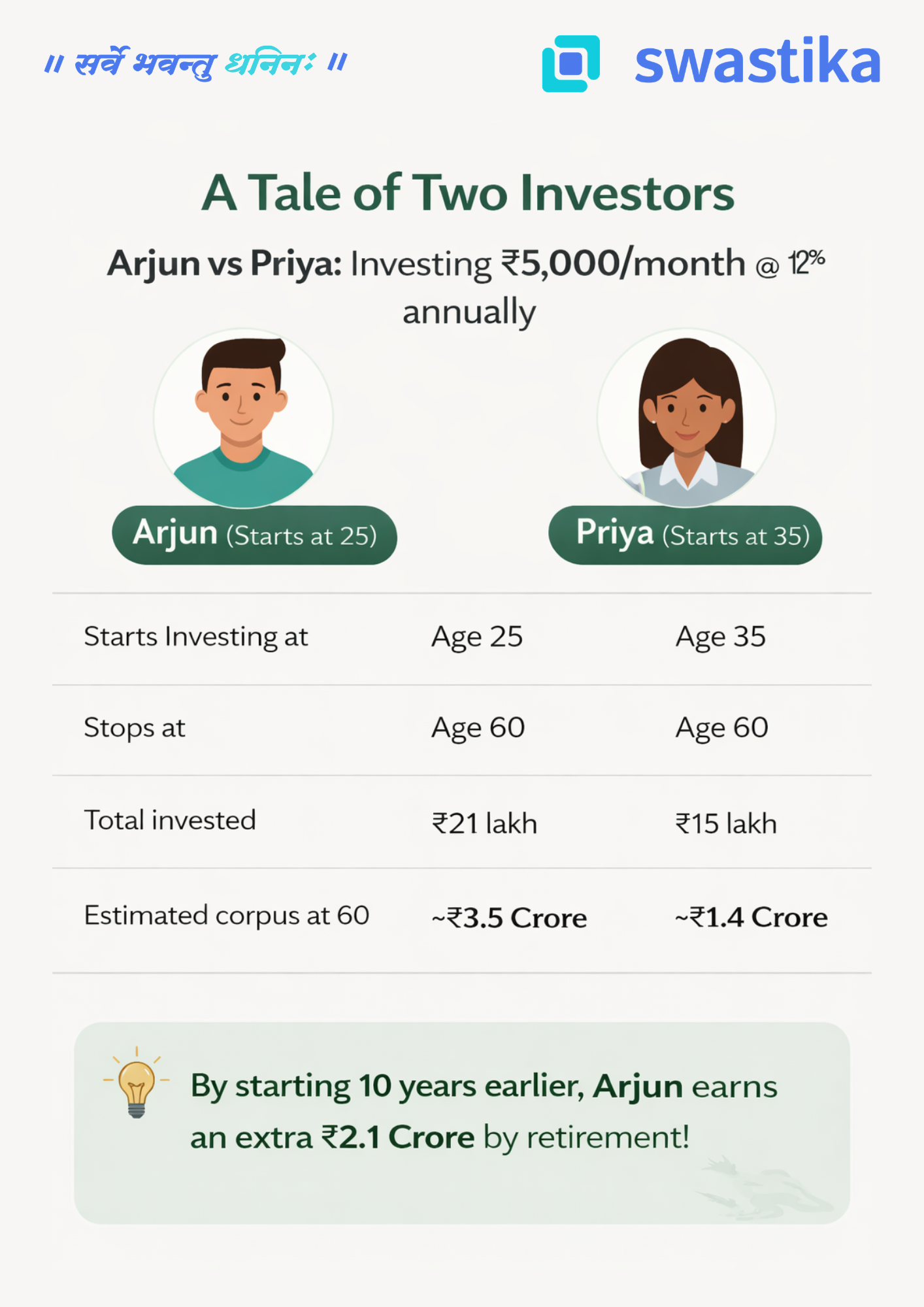

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

.webp)

RBI Ends PIDF Scheme: Why It’s a Big Negative for Paytm 🚨

Summary

- RBI has not extended the PIDF scheme beyond December 2025

- PIDF incentives contributed meaningfully to Paytm’s operating profitability

- Ending of subsidies may pressure Paytm’s payment margins

- Market sentiment has turned cautious in the short term

- Long term impact depends on Paytm’s ability to diversify revenue streams

RBI Ends PIDF Scheme: Why It’s a Big Negative for Paytm 🚨

India’s digital payments story has been one of the strongest structural growth themes of the last decade. At the centre of this ecosystem are fintech players like Paytm, which played a key role in expanding merchant payment infrastructure across urban and rural India.

However, a recent regulatory development has raised concerns among investors.

The Reserve Bank of India has ended the Payments Infrastructure Development Fund scheme after December 2025, with no announcement of an extension so far. For Paytm, this development is being seen as a material negative.

Let us understand why this matters, how big the impact could be, and what it means for investors tracking Paytm and the broader Indian markets.

Understanding the PIDF Scheme and Its Role in Digital Payments

The Payments Infrastructure Development Fund was introduced by the RBI to accelerate the adoption of digital payments, especially in underpenetrated regions.

The scheme focused on supporting the deployment of:

- Point of Sale machines

- QR code based payment systems

- Soundbox and Aadhaar enabled payment devices

These incentives reduced the cost of merchant onboarding for payment aggregators. This allowed companies like Paytm to scale faster, particularly in Tier 3, Tier 4 and rural markets where affordability is a key constraint.

From a regulatory standpoint, PIDF aligned with RBI’s long term vision of reducing cash dependency and strengthening the digital payments backbone.

What Changed After December 2025

The PIDF scheme officially ended on 31 December 2025. Despite market expectations, there has been no confirmation of an extension or replacement framework from the RBI.

This has effectively meant:

- No fresh subsidies for payment device deployment

- Higher cost burden on fintechs and acquiring banks

- Transition from incentive driven growth to self funded expansion

For companies that were still monetising these incentives, the impact is immediate.

Why the End of PIDF Is a Big Negative for Paytm

Meaningful Contribution to Operating Profit

Market estimates suggest that PIDF related incentives accounted for roughly 20 percent of Paytm’s operating profit at one stage.

This is not core transaction revenue but incentive income that directly supported margins in the payments business. With the scheme ending, this income stream disappears.

In practical terms, Paytm now has to either absorb higher costs or slow down the pace of infrastructure expansion.

Pressure on Payment Business Margins

Paytm’s payments segment operates in a highly competitive environment with regulated pricing. Merchant discount rates remain low, and profitability depends heavily on scale and operating efficiency.

The absence of PIDF support means:

- Lower incremental margins on new merchant additions

- Higher payback period for hardware investments

- Reduced operating leverage in the short term

This explains why analysts have flagged margin pressure risk in upcoming quarters.

Investor Sentiment and Stock Market Reaction

Equity markets tend to react sharply when a predictable support factor is removed.

The uncertainty around PIDF extension has led to:

- Increased earnings visibility risk

- Reassessment of near term profitability assumptions

- Heightened volatility in Paytm stock

This is less about long term survival and more about valuation recalibration.

Impact on the Broader Indian Digital Payments Ecosystem

While Paytm is the most discussed name, the impact is broader.

- Smaller fintechs may slow expansion into low density regions

- Merchants may face higher onboarding costs

- Focus may shift from aggressive expansion to monetisation and cross selling

That said, India’s digital payment volumes continue to grow strongly, supported by UPI adoption and behavioural shifts. The structural story remains intact, even if policy support reduces.

What Investors Should Watch Going Forward

For Paytm and similar players, the next few quarters will be critical.

Key factors to track include:

- Ability to offset PIDF loss through lending and financial services

- Improvement in contribution margin from merchant subscriptions

- Cost discipline and operating efficiency

- Regulatory clarity from RBI on future payment infrastructure incentives

This is where professional research and disciplined investing matter.

How Swastika Investmart Helps Investors Navigate Such Changes

Regulatory changes can materially impact stock valuations, especially in fintech and financial services.

At Swastika Investmart, investors benefit from:

- SEBI registered research backed insights

- Timely analysis of RBI and market developments

- Tech enabled trading platforms for informed decision making

- Strong customer support and investor education initiatives

Rather than reacting emotionally to headlines, investors can rely on structured research and long term perspective.

Frequently Asked Questions

Why did RBI end the PIDF scheme?

PIDF was designed as a temporary support mechanism. With digital payments reaching scale, RBI appears to be transitioning towards market driven growth.

How much did PIDF contribute to Paytm’s profits?

Estimates suggest PIDF incentives contributed around 20 percent of operating profit during certain periods.

Is this bad for Paytm’s long term business?

It is a short to medium term headwind. Long term performance will depend on diversification into lending, subscriptions, and financial services.

Will digital payment growth in India slow down?

Unlikely. Adoption remains strong, though expansion in remote regions may moderate slightly.

Should investors exit Paytm stock immediately?

Investment decisions should be based on individual risk profile and research, not single news events.

Final Thoughts

The end of the PIDF scheme is undoubtedly a negative development for Paytm in the near term, especially from a profitability and sentiment perspective. However, it also marks a maturing phase of India’s digital payments ecosystem.

For investors, this is a reminder that regulatory awareness and quality research are critical when investing in evolving sectors like fintech.

If you are looking to invest with clarity, confidence, and credible research support, explore the tools and insights offered by Swastika Investmart.

👉 Open your trading account today

Smart investing starts with informed decisions.

.webp)

Stocks in News Today: Top Indian Market Movers on 23 January 2026: Key Developments Investors Are Tracking | Key Updates Before Union Budget

Summary

- Amagi makes history as India’s first cloud native SaaS broadcasting company to list

- Premier Energies boosts renewable capacity with a 400 MW solar cell facility

- ONGC strengthens petrochemical ambitions through strategic JV investments

- Ashoka Buildcon secures a ₹307 crore infrastructure order

- These developments highlight growth themes across tech, energy and infrastructure

Stocks in News Today: Top Indian Market Movers on 23 January 2026

Tracking stocks in news is one of the most effective ways for investors to stay ahead of short term price movements and long term trends. On 23 January 2026, several Indian companies made headlines with developments that reflect broader themes shaping the Indian economy, such as digital transformation, renewable energy expansion, infrastructure growth and global partnerships.

In this edition of stocks in news today, we look closely at Amagi, Premier Energies, ONGC and Ashoka Buildcon, explaining what the news means, why it matters, and how investors can interpret these updates in the context of Indian markets.

Why Stocks in News Matter for Indian Investors

Stocks that appear in daily market news often experience higher trading volumes and increased investor attention. Corporate actions like capacity expansion, new orders, strategic investments and stock market listings can influence valuations and sentiment.

For retail investors, understanding the business impact behind the headline is far more important than reacting to price movement alone. This approach aligns with SEBI’s emphasis on informed and responsible investing.

Amagi: A Landmark Listing for India’s SaaS Ecosystem

Amagi has entered the spotlight by becoming the first cloud native SaaS company offering end to end solutions for the broadcasting and streaming ecosystem to list on Indian stock exchanges.

This milestone is significant for multiple reasons. First, it highlights India’s growing strength in software product companies rather than only IT services. Second, Amagi operates in a fast growing segment that supports connected TV advertising, a space benefiting from rising digital consumption across India and global markets.

From an investor’s perspective, this listing represents the evolving nature of Indian capital markets, where technology driven and platform based businesses are gaining acceptance. Similar past listings in the tech space have shown that while valuations can be volatile initially, companies with scalable global business models tend to attract long term interest.

Premier Energies: Strengthening India’s Renewable Energy Push

Premier Energies announced the commissioning of a 400 MW solar photovoltaic cell manufacturing facility in Telangana. This development directly aligns with India’s renewable energy goals and the government’s focus on domestic manufacturing under initiatives such as Make in India.

Solar manufacturing capacity within India reduces dependence on imports and improves supply chain stability. For the company, this expansion enhances its ability to serve large scale solar projects and government tenders.

In market terms, renewable energy stocks often react positively to capacity additions, especially when demand visibility remains strong. Investors typically assess whether such expansions are funded responsibly and whether they improve margins over the medium term.

ONGC: Strategic Global Partnership Strengthens Energy Portfolio

ONGC has completed its equity investment in two joint ventures with Japan’s Mitsui O.S.K. Lines, acquiring a 50 percent stake in Bharat Ethane One IFSC and Bharat Ethane Two IFSC.

This move reinforces ONGC’s long term strategy of strengthening its petrochemical and downstream presence. Ethane based projects are considered important for value addition beyond crude oil exploration.

Such strategic partnerships also highlight India’s increasing integration with global energy markets. For investors, PSU stocks like ONGC often balance stable dividends with long term strategic initiatives. Regulatory oversight by SEBI and government ownership adds a layer of governance that long term investors factor into their decisions.

Ashoka Buildcon: Infrastructure Momentum Continues

Ashoka Buildcon received an order worth ₹307 crore for the construction of a bridge in Daman. Infrastructure orders remain a key growth driver for construction companies, particularly as public spending on roads, bridges and urban development continues.

Order wins improve revenue visibility and often support stock sentiment, especially when the company maintains a healthy order book and execution track record.

For investors, infrastructure stocks are typically evaluated based on execution capability, balance sheet strength and cash flow management. News like this reinforces confidence in sector momentum rather than serving as a standalone trigger.

Broader Market Context and Sectoral Impact

The stocks in news today reflect three powerful themes in Indian markets: digital transformation, clean energy expansion and infrastructure development. These sectors have received consistent policy support and investor interest.

While short term price reactions may vary depending on broader market sentiment, such developments often shape medium to long term narratives. In volatile or range bound markets, stock specific news tends to drive relative outperformance.

How Investors Can Use Stocks in News Effectively

Instead of chasing headlines, investors can use stocks in news as a starting point for deeper analysis. Questions worth asking include how the development impacts revenue, margins, debt and long term competitiveness.

SEBI registered brokers with strong research capabilities help investors bridge this gap between news and informed decision making.

Why Swastika Investmart Helps Investors Stay Ahead

Swastika Investmart, a SEBI registered stockbroker, provides curated stock insights, real time market updates, and in depth research tools tailored for Indian investors. With tech enabled trading platforms and a strong focus on investor education, Swastika supports both beginners and experienced traders in navigating market news responsibly.

From daily stocks in news analysis to sector wise research, Swastika Investmart empowers clients to make decisions based on data, not noise.

Frequently Asked Questions

What does stocks in news mean in the stock market?

Stocks in news refer to companies impacted by significant developments such as orders, expansions, listings or strategic investments that may influence stock performance.

Do stocks in news always move sharply?

Not necessarily. Price movement depends on market sentiment, valuation and the actual financial impact of the news.

Is it safe to invest based only on stock news?

No. Investors should combine news analysis with fundamentals, technical levels and risk assessment.

Are renewable energy stocks good for long term investment?

Renewable energy remains a strong long term theme in India, but stock selection and valuation discipline are important.

Conclusion

The stocks in news today on 23 January 2026 highlight how Indian companies are expanding across technology, renewable energy, infrastructure and global partnerships. These developments reflect the evolving strength of the Indian economy and capital markets.

For investors looking to act on market insights with confidence, having the right research partner makes all the difference.

👉 Open your trading account with Swastika Investmart

Stay informed. Stay disciplined. Invest smarter.

.webp)

Market Set-Up for Indian Stock Market on 23 January 2026

Summary

- Global markets provide mixed cues while US indices remain supportive

- FIIs continue selling in cash markets but derivatives data signals range bound activity

- Nifty respects its 200 DMA with key support near 25,000

- Bank Nifty remains sideways amid resistance near 60,000

- Volatility cools ahead of key events, keeping traders selective

Market Set-Up for Indian Stock Market on 23 January 2026

As Indian equities prepare for trade on 23 January 2026, investors and traders are navigating a market shaped by mixed global cues, cautious institutional activity, and technically defined levels on benchmark indices. With Budget season approaching and volatility gradually cooling, market participants are focusing more on data driven strategies rather than directional bets.

This market set-up analysis provides a clear view of global trends, FII DII activity, derivatives positioning, and technical outlook for Nifty and Bank Nifty, helping traders plan the day with clarity and confidence.

Global Market Cues and Their Impact on India

Overnight, US equity markets closed higher, with the Dow Jones gaining over 300 points. This indicates resilience in global risk appetite despite lingering concerns around interest rates and macro data. Dow futures also traded marginally positive, suggesting stability rather than aggressive optimism.

Asian markets opened on a mixed note, reflecting cautious sentiment ahead of key economic triggers. For Indian markets, the Gift Nifty trading around 15 points lower signals a flat to mildly negative opening, rather than a sharp gap move.

In real market scenarios, such mixed global cues often result in a range bound opening where domestic factors and stock specific triggers dominate the session.

FII and DII Activity Explained in Simple Terms

Foreign Institutional Investors remained net sellers in the cash market, offloading shares worth around ₹2,550 crore. Domestic Institutional Investors, however, continued to support the market with net buying of over ₹4,200 crore, resulting in a positive net institutional flow.

This pattern has been consistent in recent sessions. FIIs remain cautious due to global uncertainty, while DIIs such as mutual funds and insurance companies are selectively accumulating quality stocks on dips.

For retail investors, this signals that while short term volatility may persist, long term domestic confidence in Indian equities remains intact.

Derivatives and Volatility Snapshot

In the F&O segment, the Nifty Put Call Ratio has improved to 0.87 from 0.78, indicating slightly better put writing activity and reduced bearish pressure. India VIX declined by over 3 percent to 13.78, reflecting a cooling volatility environment.

Lower volatility often translates into range based trading, where option strategies like spreads and hedged positions tend to perform better than aggressive naked trades.

The highest open interest for the January expiry remains concentrated at 26,000 Call and 25,000 Put, while the maximum pain level stands near 25,400. This suggests that the index may oscillate within a defined band unless a strong trigger emerges.

What FII Derivative Positions Are Signaling

FII data in index derivatives presents a mixed picture. While there is fresh addition in call longs and put shorts, futures positions show higher short additions compared to longs.

This combination generally indicates cautious optimism rather than outright bullishness. FIIs appear to be positioning for limited upside while protecting against downside risks.

Such behaviour is typical ahead of major events like the Union Budget, where participants prefer to stay hedged rather than directional.

Technical Outlook for Nifty

Nifty has shown resilience by respecting its 200 day moving average after a sharp fall in previous sessions. This level often acts as a strong psychological and technical support for long term investors.

Immediate resistance for Nifty lies near 25,450 followed by 25,600. A decisive breakout above these levels could invite fresh momentum buying. On the downside, supports are placed at 25,140, 25,000 and 24,900.

For traders, this means buying near support with strict stop losses may offer better risk reward than chasing breakouts in a low volatility environment.

Bank Nifty Trend and Key Levels

Bank Nifty continues to remain sideways within a broad range of 58,700 to 60,200. This reflects indecision among participants as banking stocks digest previous gains and await fresh triggers.

Immediate hurdles are seen at 59,500 and 60,000, while strong support exists near 58,700 and 58,200. Unless the index decisively moves out of this range, stock specific opportunities in private and PSU banks may offer better trading setups.

How Traders and Investors Can Approach the Day

In practical terms, a market like this rewards discipline. Intraday traders may focus on range strategies, while positional traders can wait for confirmation near key levels. Long term investors should use volatility driven dips to accumulate fundamentally strong stocks, especially in sectors backed by domestic growth themes.

SEBI regulated brokers with strong research support become crucial during such phases, as accurate data interpretation can make a meaningful difference to decision making.

Why Swastika Investmart Stands Out in Such Markets

Swastika Investmart, a SEBI registered stockbroker, provides clients with in depth market research, real time derivatives data, and advanced trading platforms designed for Indian market conditions. With a strong focus on investor education and responsive customer support, Swastika empowers traders and investors to navigate volatile and range bound markets with confidence.

Whether it is understanding FII data, decoding technical levels, or planning risk managed strategies, Swastika’s research driven approach helps clients stay one step ahead.

Frequently Asked Questions

Is the Indian stock market likely to open positive on 23 January 2026?

The market is expected to open flat to mildly negative due to mixed global cues and slightly lower Gift Nifty levels.

What does a falling India VIX indicate for traders?

A lower VIX suggests reduced volatility, often leading to range bound markets and favouring option selling or spread strategies.

Why are FIIs selling while DIIs are buying?

FIIs are cautious due to global factors, while DIIs remain confident in India’s long term growth story and continue selective buying.

Which levels are crucial for Nifty today?

Support lies near 25,000, while resistance is placed around 25,450 to 25,600.

Conclusion

The market set-up for Indian stock market on 23 January 2026 points towards a cautious yet stable environment. With strong domestic institutional support, controlled volatility, and clearly defined technical levels, traders and investors have ample opportunities provided they stay disciplined and data driven.

If you are looking to trade or invest with confidence backed by expert research and reliable technology, consider opening your account with Swastika Investmart.

👉 Open your trading account now

Smart decisions begin with the right market insights.

Stocks in News Today 22 January 2026: Key Developments Investors Are Tracking | Key Updates Before Union Budget

Summary

- Eternal Ltd reported strong Q3 results with sharp profit growth, supporting positive market sentiment

- L&T strengthened its shipping JV by acquiring partner stake, improving long-term control

- Corona Remedies received EAEU-GMP certification, opening a large export opportunity

- Apollo Hospitals got CCI approval for a major stake acquisition, reinforcing its healthcare strategy

Stocks in News Today: 22 January 2026

Indian equity markets often react sharply to company-specific news, especially earnings, acquisitions, and regulatory approvals. For active traders and long-term investors alike, tracking stocks in news today helps identify short-term momentum and long-term value creation opportunities.

On 22 January 2026, several prominent names grabbed attention across sectors like cement, infrastructure, pharmaceuticals, and healthcare. Let us break down the key developments, understand their market relevance, and see how such news can influence Indian stock markets.

Why Stocks in News Matter for Indian Investors

Company announcements act as immediate triggers for price movement. Quarterly results, regulatory clearances, and strategic acquisitions directly affect future cash flows and valuations. In India, disclosures mandated by SEBI ensure transparency, allowing investors to make informed decisions.

For retail investors, news-driven stocks often present:

- Short-term trading opportunities due to volume spikes

- Medium-term rerating based on earnings visibility

- Long-term conviction when news strengthens business fundamentals

Eternal Ltd: Strong Q3 Performance Lifts Sentiment

What Happened

Eternal Ltd reported a solid Q3 performance, posting a net profit of ₹102 crore. This marks a 56.9 percent quarter-on-quarter jump from ₹65 crore and was broadly in line with CNBC TV18 estimates.

Why the Market Cares

Earnings consistency is critical in sectors linked to infrastructure and construction demand. A strong quarterly performance signals:

- Better operating efficiency

- Stable demand environment

- Improved margin management

For investors, such results often lead to positive near-term price action, especially when expectations are met or exceeded.

Broader Market Impact

Strong corporate earnings support overall market confidence. When mid to large-cap companies deliver healthy results, it reinforces the narrative of India’s economic resilience, something foreign institutional investors closely watch.

L&T: Full Control Over Shipping Subsidiary

What Happened

Larsen and Toubro completed the acquisition of 6.35 crore shares held by Sapura Nautical Power in L&T Sapura Shipping Private. As a result, the entity has become a wholly owned subsidiary of L&T.

Strategic Importance

This move simplifies the ownership structure and gives L&T full operational and strategic control. For a conglomerate with strong EPC and maritime exposure, such consolidation can:

- Improve decision-making speed

- Enhance cost efficiency

- Unlock better long-term value

Investor Perspective

Markets generally view full ownership positively when the subsidiary aligns with the parent company’s core strengths. For long-term investors, this reflects management’s confidence in the business.

Corona Remedies: Export Opportunity Opens Up

What Happened

Corona Remedies received the Eurasian Economic Union Good Manufacturing Practices certification for its finished dosage manufacturing unit in Gujarat.

Why This Is Significant

The EAEU-GMP certification allows access to markets such as Russia, Kazakhstan, and Belarus. These regions together represent a pharmaceutical market estimated at around 25 billion dollars.

Real-World Context

Indian pharma companies have historically benefited from regulatory approvals like USFDA and EU-GMP. Similarly, EAEU certification can:

- Boost export revenues

- Diversify geographic risk

- Improve brand credibility globally

For investors, regulatory approvals often act as medium-term growth catalysts rather than one-day events.

Apollo Hospitals: CCI Approval for Strategic Acquisition

What Happened

Apollo Hospitals received approval from the Competition Commission of India to acquire a 30.58 percent stake in Apollo Health for ₹1,254 crore.

Regulatory Angle

CCI approval ensures that the transaction does not harm market competition. In India, such clearances are crucial for large healthcare deals, given the sector’s growing importance.

Market Implications

Healthcare is a defensive sector with steady demand. Strategic investments within the group can:

- Strengthen integrated healthcare services

- Improve operational synergies

- Support long-term earnings stability

Investors often view regulatory clearances as the removal of uncertainty, which can positively influence valuations.

How Should Investors Track Stocks in News

News-based investing works best when combined with research and risk management. Rather than reacting emotionally, investors should ask:

- Does this news change the company’s long-term outlook

- Is the stock already pricing in the announcement

- How does it compare with sector peers

This is where structured research, timely alerts, and expert insights become valuable.

Why Swastika Investmart Stands Out

Swastika Investmart, a SEBI registered stockbroker, supports investors with:

- Strong in-house research across equity, derivatives, and commodities

- Tech-enabled trading platforms for real-time market access

- Dedicated customer support for retail and active traders

- Continuous investor education initiatives

Such tools help investors filter noise from meaningful news and make disciplined decisions.

Frequently Asked Questions

What are stocks in news today

Stocks in news are companies that have reported significant events like earnings, acquisitions, or regulatory updates that may impact their share prices.

Do stocks in news always move up

Not necessarily. Market reaction depends on expectations. Positive news already priced in can lead to muted or even negative reactions.

Is it safe to trade only based on news

News should be combined with technical and fundamental analysis to manage risk effectively.

How do Indian regulations protect investors

SEBI mandates timely disclosures, ensuring investors receive accurate and verified information.

Where can investors track reliable stock market news

SEBI registered brokers like Swastika Investmart provide curated market updates backed by research.

Conclusion

The stocks in news today for 22 January 2026 highlight how earnings growth, strategic consolidation, regulatory approvals, and export opportunities continue to shape investor sentiment in Indian markets. While news creates momentum, informed investing requires context, discipline, and reliable research.

If you are looking to track such market-moving updates with expert insights and robust tools, consider opening an account with Swastika Investmart and experience tech-enabled investing backed by trusted research.

Market Set-Up for 22 January 2026: What Indian Investors Should Watch Today

Summary

- Global cues are positive with strong US market performance and firm Asian markets

- FIIs remain net sellers in cash but show mixed signals in derivatives

- Nifty holds its 200-DMA near 25100, indicating a crucial support zone

- Bank Nifty defends 58600 with key resistance seen at higher levels

- Volatility has picked up, making risk management essential for traders

Market Set-Up for 22 January 2026: What Indian Investors Should Watch Today

Indian equity markets head into the 22 January 2026 trading session with encouraging global cues but mixed domestic signals. While overseas markets are supporting sentiment, rising volatility and cautious institutional activity suggest that traders and investors need to stay disciplined.

This market set-up analysis breaks down global trends, FII activity, derivatives data, and technical levels for Nifty and Bank Nifty in a clear and actionable manner.

Global Market Cues Supporting Sentiment

Overnight cues from international markets are largely positive, setting a constructive tone for Indian equities.

US markets ended the previous session sharply higher, with the Dow Jones gaining over 580 points. This rally was driven by renewed optimism around corporate earnings and easing concerns over near-term interest rate risks. Importantly, Dow futures continue to trade higher, indicating follow-through momentum.

Asian markets are also trading on a positive note, reflecting improved risk appetite across global equities. Adding to this, GIFT Nifty is higher by over 150 points, hinting at a firm start for Indian benchmark indices.

For Indian investors, such global alignment often leads to a positive opening, although sustainability depends on domestic participation.

Institutional Flow and Derivative Data Analysis

FII and DII Cash Market Activity

Foreign Institutional Investors remain net sellers in the cash market, with outflows of around ₹1,788 crore. In contrast, Domestic Institutional Investors stepped in as buyers, adding more than ₹4,500 crore. This divergence highlights a familiar pattern where domestic money continues to support market declines.

The net positive institutional flow provides some stability, but persistent FII selling keeps upside capped in the near term.

F&O Indicators and Volatility

The Nifty Put Call Ratio has improved to 0.78 from 0.72, suggesting some recovery in sentiment but still not indicating aggressive bullish positioning. India VIX has jumped by over 8 percent, reflecting rising uncertainty and expectations of sharp intraday moves.

Higher volatility typically favors disciplined traders rather than aggressive positional bets.

FII Positioning in Index Derivatives

FII data in index derivatives presents a mixed picture. While there is an increase in long positions in index futures and puts, there is also significant short build-up in futures and calls. This suggests hedging activity rather than outright directional conviction.

Such positioning often results in range-bound markets with sudden spikes on news or global triggers.

Technical Outlook for Nifty

Nifty has managed to defend its 200-day moving average near the 25100 mark on a closing basis. This level remains crucial for maintaining medium-term structure.

Key Resistance Levels

- 25330 remains the first hurdle on any bounce

- 25470 is a stronger resistance zone where selling pressure may emerge

A sustained move above these levels could attract fresh buying interest.

Important Support Zones

- 25000 is an immediate psychological support

- 24900 acts as a stronger base for short-term traders

As long as Nifty holds above the 200-DMA, dips may attract selective buying, especially in quality large-cap stocks.

Bank Nifty Outlook: Stability After Sharp Fall

Bank Nifty witnessed sharp selling pressure recently but managed to close above the critical support of 58600. This indicates resilience despite volatility.

Resistance Levels to Watch

- 59300 is the first supply zone

- 59600 is a higher resistance that could cap upside in the near term

Support Zones

- 58500 remains immediate support

- 58000 is a crucial level for positional traders

Banking stocks often dictate broader market direction. Stability here could help Nifty consolidate and attempt recovery.

What This Market Set-Up Means for Indian Investors

For traders, today’s market demands patience and strict risk management. Rising volatility means stop losses should be respected, and position sizing must be conservative.

For long-term investors, such phases often provide opportunities to accumulate fundamentally strong stocks at better valuations. Domestic institutional buying continues to reinforce confidence in India’s structural growth story.

From a regulatory perspective, SEBI’s robust framework ensures transparency in derivatives and cash market data, helping investors make informed decisions based on reliable disclosures.

Why Many Investors Rely on Swastika Investmart

In volatile market conditions, access to credible research and timely insights becomes essential. Swastika Investmart, a SEBI-registered brokerage, offers in-depth market research, advanced trading tools, and strong customer support.

Its focus on investor education and technology-enabled platforms helps traders and investors navigate uncertain markets with clarity and confidence.

Frequently Asked Questions

Is the Indian stock market expected to open higher on 22 January 2026?

Based on positive global cues and higher GIFT Nifty, a firm opening is likely, though volatility may persist.

Why is India VIX rising despite positive global markets?

Rising VIX indicates uncertainty due to mixed institutional positioning and upcoming global and domestic triggers.

Is Nifty’s 200-DMA an important level for investors?

Yes, holding above the 200-DMA often signals medium-term stability and attracts long-term investors.

What does mixed FII derivative data indicate?

It usually reflects hedging and range-bound expectations rather than a clear bullish or bearish view.

How should retail investors approach such markets?

Focus on risk management, avoid over-trading, and rely on quality research before taking positions.

Conclusion

The market set-up for 22 January 2026 reflects cautious optimism. Global cues are supportive, domestic institutions are providing stability, and key technical levels are holding for now. However, elevated volatility calls for disciplined trading and informed decision-making.

If you want to navigate such markets with confidence, expert research, and reliable trading tools, consider opening an account with Swastika Investmart and stay ahead with informed investing.

Q2FY26 Results Breakdown: Revenue Boom vs Margin Pressure – Eternal, Waaree & Dr Reddy’s

Key Takeaways

- Eternal saw a sharp revenue jump in Q2FY26, but profitability and margins came under pressure

- Waaree Energies delivered strong growth across revenue, margins, and profits

- Dr Reddy’s posted steady revenue and profit growth, though margins softened slightly

- The results highlight how execution and cost control are shaping market reactions

Q2FY26 Results Breakdown: Revenue Boom vs Margin Pressure – Eternal, Waaree & Dr Reddy’s

The Q2FY26 earnings season once again proved that headline revenue growth does not always translate into stronger profitability. While demand conditions remain supportive in several sectors, margin pressures, cost structures, and execution efficiency are becoming clear differentiators.

Three companies that perfectly capture this contrast are Eternal, Waaree Energies, and Dr Reddy’s Laboratories. Their Q2FY26 results reflect three very different operating realities, offering useful insights for investors trying to separate short-term noise from long-term fundamentals.

The Bigger Picture Behind Q2FY26 Earnings

The September quarter benefited from relatively stable domestic demand, improving infrastructure activity, and supportive policy conditions. At the same time, companies faced challenges such as input cost volatility, competitive pricing, and higher operating expenses.

Markets are increasingly rewarding consistency and margin discipline rather than just topline expansion. Against this backdrop, let us break down what the numbers really say.

Eternal: Revenue Surge, Profitability Takes a Hit

Eternal reported a dramatic rise in consolidated revenue from operations in Q2FY26, reaching Rs 13,590 crore compared to Rs 4,799 crore in the same quarter last year. On the surface, this looks like a blockbuster performance.

However, the story changes when we look at the bottom line.

Key Financial Takeaways

- Profit for the period declined to Rs 65 crore from Rs 176 crore year on year

- Consolidated adjusted Ebitda fell 32 percent to Rs 224 crore from Rs 330 crore

- Margin pressure remained the key concern despite strong revenue growth

What Is Driving the Gap

The sharp revenue growth suggests scale expansion, possible consolidation effects, or aggressive market capture. However, higher operating costs, pricing pressures, or integration-related expenses appear to have weighed on margins.

For investors, Eternal’s results underline an important lesson. Growth without profitability sustainability can lead to cautious market reactions, especially in a cost-sensitive environment.

Waaree Energies: Strong Growth with Improving Margins

Waaree Energies delivered one of the most impressive Q2FY26 performances among mid to large industrial players. The renewable energy major not only grew revenues but also significantly improved profitability.

Key Financial Takeaways

- Consolidated revenue rose to Rs 6,065.64 crore from Rs 3,574.38 crore

- Ebitda surged 155.29 percent to Rs 1,567.30 crore

- Ebitda margins expanded to 25.17 percent from 16.76 percent

- Profit after tax more than doubled to Rs 878.21 crore

Why Markets Are Paying Attention

Waaree’s results reflect operating leverage at work. Strong execution, better capacity utilization, and improving pricing power have translated into meaningful margin expansion.

This performance also aligns with broader market themes. Renewable energy continues to benefit from policy support, rising domestic manufacturing, and long-term visibility. For investors, Waaree Energies stands out as an example of how scale and efficiency can drive both growth and profitability.

Dr Reddy’s Laboratories: Steady Growth with Margin Moderation

Dr Reddy’s Laboratories delivered a balanced Q2FY26 performance, marked by steady growth and resilient profitability, even as margins softened slightly.

Key Financial Takeaways

- Consolidated revenue increased 9.8 percent to Rs 8,805 crore

- Ebitda rose marginally to Rs 2,351 crore from Rs 2,280 crore

- Ebitda margins declined to 26.7 percent from 28.4 percent

- Profit after tax attributable to equity holders grew 14 percent to Rs 1,437 crore

What This Means for Investors

In the pharmaceutical sector, consistency often matters more than sharp spikes. Dr Reddy’s results suggest stable demand, controlled costs, and continued focus on complex generics and regulated markets.

The slight margin dip is not unusual in a competitive global pharma environment. Importantly, profit growth remains intact, reinforcing confidence in the company’s long-term fundamentals.

Comparing the Three: What the Results Tell Us

Looking at Eternal, Waaree Energies, and Dr Reddy’s together highlights a clear market trend.

- Eternal shows that rapid expansion can strain margins if cost structures are not tightly managed

- Waaree Energies demonstrates how strong execution can convert growth into profitability

- Dr Reddy’s reflects steady compounding with manageable margin pressures

This contrast explains why stock reactions during earnings season are increasingly selective rather than broad-based.

Impact on Indian Markets

From a broader market perspective, these results reinforce three themes:

- Sectoral divergence is widening, with renewables and select manufacturing players outperforming

- Margin visibility is becoming as important as revenue growth

- Stock-specific analysis matters more than index-level assumptions

For Indian equity markets, this means volatility around results is likely to persist, especially for companies with stretched valuations or inconsistent margins.

Why Research-Driven Investing Matters

Earnings numbers tell only part of the story. Understanding what drives those numbers is where real investing insight lies.

A SEBI-registered platform like Swastika Investmart helps investors navigate earnings seasons with:

- In-depth fundamental research

- Advanced analytical tools

- Tech-enabled trading platforms

- Strong customer support and ongoing investor education

Such support becomes especially valuable when markets react sharply to quarterly results.

Frequently Asked Questions

Why did Eternal’s profit fall despite higher revenue?

Higher operating costs and margin pressure offset the benefits of strong topline growth.

What made Waaree Energies’ Q2FY26 results stand out?

Significant margin expansion and more than doubling of profits driven by operational efficiency.

Is Dr Reddy’s margin decline a concern?

The decline is moderate and does not materially impact the company’s long-term earnings stability.

Do these results impact the broader market?

The impact is largely stock-specific, though strong sectors can influence overall sentiment.

How should investors approach such mixed earnings?

By focusing on fundamentals, margin trends, and long-term growth visibility rather than short-term reactions.

Final Thoughts

The Q2FY26 results of Eternal, Waaree Energies, and Dr Reddy’s highlight a crucial investing truth. Revenue growth attracts attention, but margin discipline and execution decide sustainability.

As earnings season continues, staying informed and analytical is key. If you want access to credible research, reliable insights, and a trusted investing platform, consider opening an account with Swastika Investmart.

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App