Price Of South Indian Bank Share: 200 DMA Breakouts Across Nifty500 Stocks

Key Takeaways

- Fifteen Nifty500 stocks closed below their 200-day moving average on July 22.

- The data table below shows the 200 DMA and last price for each stock, including the south indian bank stock price.

- A move below the 200 DMA signals potential long-term trend weakness, warranting cautious positioning.

- For deeper insights, use Swastika's Sarthi AI stock assistant to analyse individual stock setups.

On July 22, 2026, fifteen Nifty500 stocks closed below their 200-day moving averages, testing the durability of long-term trend lines. If you are watching the price of south indian bank share, this cross below the 200 DMA is a caution signal suggesting potential downside pressure ahead. stockedge's technical scan data confirms the breadth of this signal across sectors, from fintech to industrials. The breadth suggests that the signal is not an isolated blip but a market-wide reflection of medium-to-long-term trend weakness that retail investors should respect rather than ignore.

The 200-day moving average (200 DMA) is one of the most widely watched long-term trend indicators. When prices trade below this line, it often implies that the stock is hovering under its longer-run momentum, and trend-following strategies may become less reliable. For investors, the takeaway is not fear but calibrated risk management–identify which names have genuine catalysts or improving fundamentals and which ones may simply be undergoing a cyclical pullback. As always, context matters: sector dynamics, liquidity, and macro cues can influence how long a 200 DMA breach persists.

Below is the list of the 15 stocks that crossed below their 200 DMA on July 22, with their 200 DMA levels and last traded prices (LTP) in Rs. Use this snapshot to assess which names are marginally oversold versus those that may require more time to stabilize.

Which Stocks Crossed Below Their 200 DMA On July 22 In The Nifty500?

| Stock | 200 DMA (Rs) | LTP (Rs) |

|---|---|---|

| Ola Electric Mobility | Rs 37.99 | Rs 36.67 |

| south indian bank stock price | Rs 854.16 | Rs 827.55 |

| Chalet Hotels | Rs 838.7 | Rs 822.45 |

| Bank Of India | Rs 146.38 | Rs 143.99 |

| Berger Paints India | Rs 502.93 | Rs 496.45 |

| Eris Lifesciences | Rs 1456.07 | Rs 1440.6 |

| sobha developers stock price | Rs 1441.13 | Rs 1426 |

| 360 One Wam | Rs 1102.61 | Rs 1093.6 |

| Urban Company | Rs 131.77 | Rs 130.88 |

| jubilant pharmova stock | Rs 994.1 | Rs 989 |

| lic housing finance stock price | Rs 541.3 | Rs 538.6 |

| ZF Commercial Vehicle Control Systems India | Rs 2379.06 | Rs 2367.2 |

| nmdc steel stock | Rs 42.44 | Rs 42.24 |

| Graphite India | Rs 631.96 | Rs 629.55 |

| hdb financial services | Rs 707.96 | Rs 707.20 |

From the table, the breadth of the signal is evident–across consumer, financials, industrials, and tech-adjacent names, the common thread is price action trading under the long-term trend line. For example, south indian bank stock price shows a 200 DMA of Rs 854.16 with an LTP of Rs 827.55, placing it roughly 3.1% below the long-run average. This kind of gap needs to be contextualized with fundamentals, liquidity, and catalysts. Some stocks may stabilize around the 200 DMA, while others could extend the breach if macro conditions worsen or earnings disappoint.

Understanding The 200 DMA And Long-Term Trend Signals For Retail Investors

The 200 DMA is a smoothed view of a stock’s price action over roughly the last 40–60 trading sessions, depending on market conditions. When the price crosses below the 200 DMA, many traders interpret it as a signal that the stock’s medium-to-long-term momentum has shifted to the downside. However, it is not a standalone sell signal. Investors should confirm with other indicators, such as price action around support levels, relative strength indices, and volume patterns. The goal is to separate meaningful trend signals from typical noise in daily fluctuations.

In a multi-name environment like the Nifty500, a broad breach across several stocks can indicate macro- or sector-level dynamics rather than a problem with any single company. The 15-name list includes a mix of consumer cycles, rate-sensitive financials, and growth-oriented names. This breadth underscores the importance of diversification, position sizing, and a disciplined risk framework, especially for retail investors who may not have the same access to sophisticated hedging tools as institutions.

Price Of South Indian Bank Share Signals In The 200 DMA Breakouts Across Nifty500

The focus on price of south indian bank share on this date highlights how a single name can reflect broader market signals while also presenting its own idiosyncrasies. For this stock, the 200 DMA sits at Rs 854.16 and the latest trade is Rs 827.55, a gap of about 3.1% below the long-term benchmark. Such gaps can be a prelude to a test of support levels or a shift in investor sentiment, depending on news flow and earnings cadence. Investors should examine liquidity, promoter actions, and sector-specific catalysts before scaling exposure.

Beyond the specifics of one stock, the list demonstrates that 200 DMA breaches can occur across sectors in a relatively short time window. Retail investors should avoid overgeneralizing from a handful of names and instead use these signals as a starting point for deeper stock-by-stock due diligence. If you want a structured framework to analyse these signals quickly, consider using a decision-support tool that integrates moving-average crossovers with fundamental filters.

Investment Implications And Risk Management For Retail Investors

Crosses below the 200 DMA should prompt traders to reassess risk and review their allocations. Some investors might reduce exposure to weaker names or those with fragile fundamentals, while others could wait for price action to reassert the long-term trend before adding. The key is to align position sizing with risk tolerance. A practical approach is to apply defined stops, use trailing stops as prices move, and avoid layering new buys into a broad down-move without clear catalysts.

In practice, the 200 DMA breach is best used as a prompt to re-check thesis and ensure your portfolio is not susceptible to a broad-based drawdown. It’s also a reminder that during periods of relative market stress, liquidity can become a constraint; the more liquid your holdings, the easier it is to manage downside without forced exits. As always, a structured watchlist, regular portfolio reviews, and a clear exit plan help preserve capital over the long run.

Frequently Asked Questions

How many stocks crossed below their 200-day moving average on July 22, 2026?

Fifteen stocks in the Nifty500 pack closed below their 200 DMA on July 22, according to stockedge's technical scan data.

Which stocks crossed the 200 DMA on that date?

The 15 stocks were Ola Electric Mobility, south indian bank stock price, Chalet Hotels, Bank Of India, Berger Paints India, Eris Lifesciences, sobha developers stock price, 360 One Wam, Urban Company, jubilant pharmova stock, lic housing finance stock price, ZF Commercial Vehicle Control Systems India, nmdc steel stock, Graphite India, and hdb financial services.

What does trading below the 200 DMA imply for long-term trends?

Trading below the 200 DMA typically signals that a stock is below its long-term trend, suggesting potential downside risk or a shift in momentum. It is a caution signal that should be considered in conjunction with other indicators and fundamentals.

Where can I get deeper stock analysis on these signals?

You can use Swastika's Sarthi AI stock assistant for institutional-level research on any stock or index. It helps model scenarios and compare moving-average signals quickly.

What is the significance of the data source for these signals?

The signals come from stockedge's technical scan data, which tracks closing prices relative to the 200 DMA to identify negative breakout patterns in the Nifty500 pack.

Conclusion

For the retail investor, these 200 DMA breakouts are a reminder that long-term trend lines matter. They provide a framework to gauge risk, but they don’t replace judgment about company fundamentals, valuations, or macro catalysts. The presence of a broad list signals caution, but it also creates an opportunity to sharpen your process–to separate names with compelling value from those likely to drift with the crowd.

Next steps: refine your watchlist using the 200 DMA as a baseline, apply a robust risk management framework, and consider using Swastika's Sarthi AI stock assistant to explore individual stock setups in greater depth before committing capital. This disciplined approach helps you stay prepared for the next wave of market moves rather than being blindsided by momentum shifts.

Latest Articles

Price Of South Indian Bank Share: 200 DMA Breakouts Across Nifty500 Stocks

Key Takeaways

- Fifteen Nifty500 stocks closed below their 200-day moving average on July 22.

- The data table below shows the 200 DMA and last price for each stock, including the south indian bank stock price.

- A move below the 200 DMA signals potential long-term trend weakness, warranting cautious positioning.

- For deeper insights, use Swastika's Sarthi AI stock assistant to analyse individual stock setups.

On July 22, 2026, fifteen Nifty500 stocks closed below their 200-day moving averages, testing the durability of long-term trend lines. If you are watching the price of south indian bank share, this cross below the 200 DMA is a caution signal suggesting potential downside pressure ahead. stockedge's technical scan data confirms the breadth of this signal across sectors, from fintech to industrials. The breadth suggests that the signal is not an isolated blip but a market-wide reflection of medium-to-long-term trend weakness that retail investors should respect rather than ignore.

The 200-day moving average (200 DMA) is one of the most widely watched long-term trend indicators. When prices trade below this line, it often implies that the stock is hovering under its longer-run momentum, and trend-following strategies may become less reliable. For investors, the takeaway is not fear but calibrated risk management–identify which names have genuine catalysts or improving fundamentals and which ones may simply be undergoing a cyclical pullback. As always, context matters: sector dynamics, liquidity, and macro cues can influence how long a 200 DMA breach persists.

Below is the list of the 15 stocks that crossed below their 200 DMA on July 22, with their 200 DMA levels and last traded prices (LTP) in Rs. Use this snapshot to assess which names are marginally oversold versus those that may require more time to stabilize.

Which Stocks Crossed Below Their 200 DMA On July 22 In The Nifty500?

| Stock | 200 DMA (Rs) | LTP (Rs) |

|---|---|---|

| Ola Electric Mobility | Rs 37.99 | Rs 36.67 |

| south indian bank stock price | Rs 854.16 | Rs 827.55 |

| Chalet Hotels | Rs 838.7 | Rs 822.45 |

| Bank Of India | Rs 146.38 | Rs 143.99 |

| Berger Paints India | Rs 502.93 | Rs 496.45 |

| Eris Lifesciences | Rs 1456.07 | Rs 1440.6 |

| sobha developers stock price | Rs 1441.13 | Rs 1426 |

| 360 One Wam | Rs 1102.61 | Rs 1093.6 |

| Urban Company | Rs 131.77 | Rs 130.88 |

| jubilant pharmova stock | Rs 994.1 | Rs 989 |

| lic housing finance stock price | Rs 541.3 | Rs 538.6 |

| ZF Commercial Vehicle Control Systems India | Rs 2379.06 | Rs 2367.2 |

| nmdc steel stock | Rs 42.44 | Rs 42.24 |

| Graphite India | Rs 631.96 | Rs 629.55 |

| hdb financial services | Rs 707.96 | Rs 707.20 |

From the table, the breadth of the signal is evident–across consumer, financials, industrials, and tech-adjacent names, the common thread is price action trading under the long-term trend line. For example, south indian bank stock price shows a 200 DMA of Rs 854.16 with an LTP of Rs 827.55, placing it roughly 3.1% below the long-run average. This kind of gap needs to be contextualized with fundamentals, liquidity, and catalysts. Some stocks may stabilize around the 200 DMA, while others could extend the breach if macro conditions worsen or earnings disappoint.

Understanding The 200 DMA And Long-Term Trend Signals For Retail Investors

The 200 DMA is a smoothed view of a stock’s price action over roughly the last 40–60 trading sessions, depending on market conditions. When the price crosses below the 200 DMA, many traders interpret it as a signal that the stock’s medium-to-long-term momentum has shifted to the downside. However, it is not a standalone sell signal. Investors should confirm with other indicators, such as price action around support levels, relative strength indices, and volume patterns. The goal is to separate meaningful trend signals from typical noise in daily fluctuations.

In a multi-name environment like the Nifty500, a broad breach across several stocks can indicate macro- or sector-level dynamics rather than a problem with any single company. The 15-name list includes a mix of consumer cycles, rate-sensitive financials, and growth-oriented names. This breadth underscores the importance of diversification, position sizing, and a disciplined risk framework, especially for retail investors who may not have the same access to sophisticated hedging tools as institutions.

Price Of South Indian Bank Share Signals In The 200 DMA Breakouts Across Nifty500

The focus on price of south indian bank share on this date highlights how a single name can reflect broader market signals while also presenting its own idiosyncrasies. For this stock, the 200 DMA sits at Rs 854.16 and the latest trade is Rs 827.55, a gap of about 3.1% below the long-term benchmark. Such gaps can be a prelude to a test of support levels or a shift in investor sentiment, depending on news flow and earnings cadence. Investors should examine liquidity, promoter actions, and sector-specific catalysts before scaling exposure.

Beyond the specifics of one stock, the list demonstrates that 200 DMA breaches can occur across sectors in a relatively short time window. Retail investors should avoid overgeneralizing from a handful of names and instead use these signals as a starting point for deeper stock-by-stock due diligence. If you want a structured framework to analyse these signals quickly, consider using a decision-support tool that integrates moving-average crossovers with fundamental filters.

Investment Implications And Risk Management For Retail Investors

Crosses below the 200 DMA should prompt traders to reassess risk and review their allocations. Some investors might reduce exposure to weaker names or those with fragile fundamentals, while others could wait for price action to reassert the long-term trend before adding. The key is to align position sizing with risk tolerance. A practical approach is to apply defined stops, use trailing stops as prices move, and avoid layering new buys into a broad down-move without clear catalysts.

In practice, the 200 DMA breach is best used as a prompt to re-check thesis and ensure your portfolio is not susceptible to a broad-based drawdown. It’s also a reminder that during periods of relative market stress, liquidity can become a constraint; the more liquid your holdings, the easier it is to manage downside without forced exits. As always, a structured watchlist, regular portfolio reviews, and a clear exit plan help preserve capital over the long run.

Frequently Asked Questions

How many stocks crossed below their 200-day moving average on July 22, 2026?

Fifteen stocks in the Nifty500 pack closed below their 200 DMA on July 22, according to stockedge's technical scan data.

Which stocks crossed the 200 DMA on that date?

The 15 stocks were Ola Electric Mobility, south indian bank stock price, Chalet Hotels, Bank Of India, Berger Paints India, Eris Lifesciences, sobha developers stock price, 360 One Wam, Urban Company, jubilant pharmova stock, lic housing finance stock price, ZF Commercial Vehicle Control Systems India, nmdc steel stock, Graphite India, and hdb financial services.

What does trading below the 200 DMA imply for long-term trends?

Trading below the 200 DMA typically signals that a stock is below its long-term trend, suggesting potential downside risk or a shift in momentum. It is a caution signal that should be considered in conjunction with other indicators and fundamentals.

Where can I get deeper stock analysis on these signals?

You can use Swastika's Sarthi AI stock assistant for institutional-level research on any stock or index. It helps model scenarios and compare moving-average signals quickly.

What is the significance of the data source for these signals?

The signals come from stockedge's technical scan data, which tracks closing prices relative to the 200 DMA to identify negative breakout patterns in the Nifty500 pack.

Conclusion

For the retail investor, these 200 DMA breakouts are a reminder that long-term trend lines matter. They provide a framework to gauge risk, but they don’t replace judgment about company fundamentals, valuations, or macro catalysts. The presence of a broad list signals caution, but it also creates an opportunity to sharpen your process–to separate names with compelling value from those likely to drift with the crowd.

Next steps: refine your watchlist using the 200 DMA as a baseline, apply a robust risk management framework, and consider using Swastika's Sarthi AI stock assistant to explore individual stock setups in greater depth before committing capital. This disciplined approach helps you stay prepared for the next wave of market moves rather than being blindsided by momentum shifts.

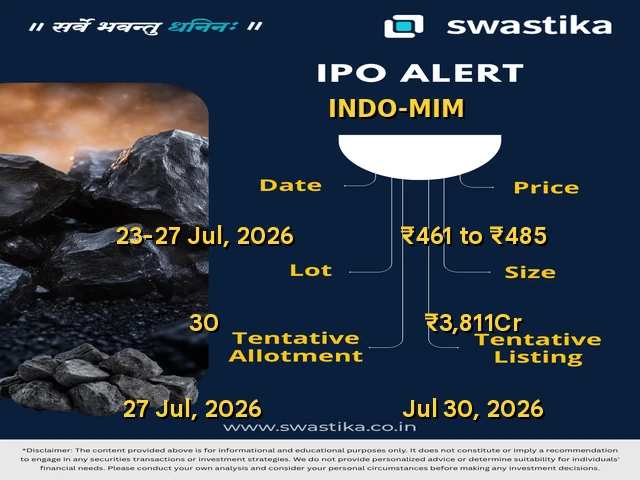

INDO-MIM Limited IPO: Apply or Watch the Listing?

Key Takeaways

- INDO-MIM Limited IPO opens 23–27 Jul 2026 with a price band of ₹461–₹485 and an aggregate issue size up to ₹3,811 Cr.

- OFS dominates the offer (about 87%), with Fresh Issue ₹499 Cr; Listing on 30 Jul 2026.

- GMP is not available yet; listing gain signals are uncertain.

- FY2026 shows Revenue ₹4,320.70 Cr and PAT ₹533.54 Cr, with Revenue YoY growth +28.1% and PAT YoY growth +25.9%.

INDO-MIM Limited: Company Background And Business

INDO-MIM Limited is a main-board IPO of 7,86,00,300 equity shares of the face value ₹1, aggregating up to ₹3,811 Crores. The issue is priced at ₹461 to ₹485. The minimum order quantity is 30. The IPO opens on Thu, 23 Jul 2026, and closes on Mon, 27 Jul 2026. MUFG Intime India Pvt.Ltd. is the registrar for the IPO. The shares are proposed to be listed on BSE and NSE.

INDO-MIM Limited IPO Details: Price Band, Lot Size, And Dates

Price band: ₹461 to ₹485 per share. Lot size: 30 shares. Issue size: 7,86,00,300 shares (aggregating up to ₹3,811 Cr). Open date: 23 Jul 2026. Close date: 27 Jul 2026. Listing date: Thu, Jul 30 2026. Exchange: BSE, NSE. Issue type: Bookbuilding IPO. Fresh issue: 1,03,09,278 shares (₹499 Cr). OFS: 6,82,91,022 shares (₹3,311 Cr). Registrar: To be announced. Lead Manager: To be announced. Market Cap: ₹23,981.42 Cr. Quotas: QIB up to 50% of Net Offer; NII not less than 15% of Net Offer; Retail not less than 35% of Net Offer. Min Investment: To be announced.

| Financials (₹ Cr) | 31 Mar 2026 | 31 Mar 2025 |

|---|---|---|

| Revenue | ₹4,320.70 | ₹3,373.97 |

| PAT | ₹533.54 | ₹423.73 |

| Net Worth | ₹2,819.55 | ₹2,199.43 |

| Borrowings | ₹1,090.49 | ₹1,247.20 |

Revenue YoY growth: +28.1% | PAT YoY growth: +25.9%

FY2026 Revenue: ₹4,320.70 Cr; PAT: ₹533.54 Cr; Net Worth: ₹2,819.55 Cr; Borrowings: ₹1,090.49 Cr. FY2025 Revenue: ₹3,373.97 Cr; PAT: ₹423.73 Cr; Net Worth: ₹2,199.43 Cr; Borrowings: ₹1,247.20 Cr.

GMP data: Not available yet. Investors should be aware that there is no real-time listing gains signal to rely on. Subscriptions data (Retail, NII, QIB) are 0x at this stage; actual numbers will be updated as the process proceeds.

To explore deeper stock analytics, use Swastika's Sarthi AI stock assistant.

INDO-MIM Limited IPO Valuation: Is The ₹461-₹485 Band Justified?

The company reports strong YoY growth in FY2026 (Revenue up 28.1%, PAT up 25.9%), but the IPO structure is dominated by OFS (around 87% of the total issue), which limits fresh capital for the company and could inflate demand from existing shareholders. The price band sits at ₹461-₹485, with a corresponding market cap indicating a high valuation relative to earnings. Investors should benchmark against peers and consider the post-IPO liquidity and potential price movement on listing day.

INDO-MIM Limited Risks: What Could Go Wrong?

- OFS-heavy issue reduces fresh capital for the company and could affect post-listing price dynamics.

- GMP data is not available yet, leaving listing-day gains uncertain.

- Lead Manager and Registrar details are not disclosed in the available data, which could impact investor confidence and process clarity.

How To Apply For INDO-MIM Limited IPO Via UPI/ASBA

To apply, you’ll need a Demat account with a broker and access to IPO bidding. You can choose UPI-based bidding or the ASBA route through your bank. Steps typically include selecting the INDO-MIM Limited IPO, choosing the bid price within the ₹461–₹485 band, entering the number of shares (minimum 30), and confirming the bid with UPI or ASBA. The bank or broker blocks funds for ASBA, or debits the UPI-linked bank account for UPI bids, only on allotment. After the close, monitor allotment news and listing day actions. For precise steps, follow the official IPO portal and your broker’s instructions as processes may vary.

Open the Sarthi AI stock assistant for deeper insights: Swastika's Sarthi AI stock assistant.

Min investment and lead-manager details will be announced soon.

Frequently Asked Questions

Is INDO-MIM Limited IPO worth applying for at ₹461-₹485?

The company shows strong YoY growth (Revenue +28.1%, PAT +25.9%), but the issue is heavily dominated by OFS (about 87%), and there is no GMP data yet. This makes the decision risk-adjusted and dependent on your risk tolerance and post-listing plan.

What does GMP not available yet mean for listing gains?

GMP data is not available yet, so there is no reliable signal about listing gains. Investors should rely on fundamentals and price-band dynamics rather than speculative listing pops.

What are the allotment odds for retail investors in the INDO-MIM Limited IPO?

Retail quota is not less than 35% of Net Offer, but exact allotment odds depend on the final subscription mix. No oversubscription data is provided yet, so odds cannot be precisely estimated.

When is INDO-MIM Limited listing on BSE/NSE?

The listing date is 30 July 2026, with open dates from 23 July to 27 July 2026.

What is the minimum investment for the INDO-MIM Limited IPO?

Min investment: To be announced. The minimum bid quantity is 30 shares per lot.

Conclusion

INDO-MIM Limited's IPO presents a growth-backed issuer with a heavy OFS component, making the immediate price dynamics uncertain and the post-listing performance dependent on demand beyond new capital inflow. For retail investors with a defined risk tolerance and a post-listing plan, this IPO merits watchful consideration rather than an automatic buy. Watch for GMP movements and how the market absorbs the issue on listing day before deciding to apply or skip.

Watchlist – the right approach here is to wait for GMP signals and listing-day reactions before committing capital.

Ofss Share Price Outlook After Oracle Financial Services Historic Q1 2026 Results

Key Takeaways

- Investors see a historic Q1 2026: consolidated net income rose 121% to Rs 1,416 crore and revenue from operations rose 69% to Rs 3,125 crore.

- Products revenue jumped 75% YoY to Rs 2,936 crore while services revenue rose 6% to Rs 189 crore.

- Strategic client wins and AI-first modernization underpin a strong growth narrative across regions including the US, Mexico, Japan, and India.

- For retail investors, the focus is on durability of earnings growth and the potential response of the ofss share price.

In a quarter that many will remember, Oracle Financial Services Software posted a historic Q1 2026, setting new benchmarks for profitability and top-line growth. The numbers are more than just headline figures; they map to a shift in the business model driven by an AI-first strategy and ongoing product modernization. For investors, the key question is not just the absolute numbers but whether this momentum is sustainable and how it could influence the ofss share price in the near term.

Consolidated net income rose 121% year-on-year to Rs 1,416 crore, while revenue from operations rose 69% year-on-year to Rs 3,125 crore. Operating income surged 123% to Rs 1,861 crore. The products business revenue was Rs 2,936 crore, marking a 75% increase during the quarter, while revenue from the services business rose 6% to Rs 189 crore. The quarter under review ended June 30, 2026. This trio of numbers frames a story of margin expansion alongside top-line growth, with the AI-first approach at the core of the modernization effort.

Ofss Share Price After Historic Q1 2026 Results

The headline figures alone don’t tell the full story. The consolidated PAT and operating profit growth imply a stronger earnings trajectory, which can influence the market’s assessment of the ofss share price as investors weigh the sustainability and breadth of the expansion. In this quarter, Oracle Financial Services Software not only posted impressive profitability but also demonstrated that its product modernization strategy is translating into meaningful revenue gains across core platforms.

| Metric | Value |

|---|---|

| Consolidated Net Income | Rs 1,416 crore |

| Revenue From Operations | Rs 3,125 crore |

| Operating Income | Rs 1,861 crore |

| Products Revenue | Rs 2,936 crore |

| Services Revenue | Rs 189 crore |

These figures reflect robust profit growth and a product-centric revenue mix, with the products segment delivering a 75% year-on-year gain while services show a more modest, yet positive, 6% expansion. The quarter under review ended June 30, 2026, a date that regulators note in filings and that the market is watching for indications of how this trajectory translates into sustained earnings power.

Q1 2026 Performance: Net Income, Revenue, And Segment Breakup

The quarter’s profit and revenue growth is further broken down into segments. The products business delivered Rs 2,936 crore in revenue, a 75% YoY rise, underscoring the company’s continued strength in modernizing product lines for financial institutions. The services segment grew to Rs 189 crore, up 6% YoY, showing resilience even as product-driven revenue remains the dominant driver. Net income rose to Rs 1,416 crore, up 121% YoY, while operating income climbed to Rs 1,861 crore, up 123% YoY. These numbers point toward a powerful combination of top-line momentum and improving margins.

Tabled below is a snapshot of the quarter’s key numbers to help you compare the scale and mix quickly:

| Metric | Value (Rs Crore) |

|---|---|

| Consolidated Net Income | Rs 1,416 |

| Revenue From Operations | Rs 3,125 |

| Operating Income | Rs 1,861 |

| Products Revenue | Rs 2,936 |

| Services Revenue | Rs 189 |

Major Client Wins And Global Adoption Driving Growth

Beyond the headline numbers, the quarter highlighted meaningful client wins and regional adoption that validate the company’s go-to-market strategy. During the period, one of the largest vacation ownership companies in the United States signed an agreement for Oracle Financial Services Lending and Leasing Cloud Service to support its digital transformation initiatives. A reputed Mexican company signed an agreement to implement Oracle Financial Services Analytical Applications to enhance its analytical capabilities. A leading U.S.-based company substantially increased its licensed account volume, becoming one of the largest users of Oracle Financial Services Lending and Leasing. A Japanese bank signed an agreement to adopt Oracle Accounting Foundation and Oracle Financial Services Analytical Applications Cloud Service, becoming one of the first customers in the region to implement these solutions. A U.S.-headquartered bank with an extensive global presence signed a strategic agreement for Oracle FLEXCUBE Banking as part of its continued investment in perpetual licenses, related solutions and transfer of personnel. A prominent U.S.-based life insurance company has continued to invest in Oracle Financial Services Analytical Applications to enhance its financial analytics capabilities. An Indian bank has expanded its investment in Oracle Banking and Oracle Financial Services solutions, reaffirming its confidence in the company; the agreement covers core banking, payments, digital banking and analytical applications.

These agreements demonstrate how the company’s AI-powered product modernization is being adopted across geographies, from North America to Asia, and reinforce the broader growth narrative built around cloud-based solutions and analytics.

AI-First Strategy And Product Modernization As Growth Drivers

The quarter’s success is attributed by management to an AI-first strategy and ongoing product modernization. The ability to deliver AI-enabled analytics and modern core banking and payments solutions has helped OFSS accelerate deal momentum and expand revenue pools. The depth and breadth of client engagements–from cloud services to digital banking and analytics–signal a strategic shift toward high-margin, subscription-like revenue streams and long-term client relationships.

As the market contemplates the implications for OFSS share price in the near term, it’s important to note that this is not a single-driver story. The AI-first approach complements the robust product lineup and expands the total addressable market. With new deals spanning the U.S., Mexico, Japan, and India, the company demonstrates a diversified revenue mix that supports sustainable growth even if consumer demand or macro headwinds shift in the short term.

What Retail Investors Should Watch Next

Investors should watch how the company translates this quarter’s profitability into free cash flow and how the product modernization cycle evolves in subsequent quarters. The pace of new client wins, particularly in strategic markets, will be a key indicator of durable growth. Additionally, investors should monitor any commentary on cross-sell opportunities within existing clients and the expansion of cloud-based offerings that could amplify margins over time.

For readers seeking deeper stock-specific insights and a data-driven framework to compare OFSS with peers, Swastika offers Swastika's Sarthi AI stock assistant to assist with institutional-grade analysis of stocks and indices. This tool can help you test scenarios, understand sensitivity to supply/demand shifts in technology adoption, and model earnings outcomes under different AI-driven growth trajectories.

Frequently Asked Questions

What were OFSS's key numbers in Q1 2026?

Consolidated net income rose 121% to Rs 1,416 crore; Revenue from operations rose 69% YoY to Rs 3,125 crore; Operating income rose 123% to Rs 1,861 crore. Products revenue was Rs 2,936 crore (75% growth) and services revenue Rs 189 crore (6% growth). The quarter ended June 30, 2026.

What drove the growth in OFSS's Q1 2026 performance?

Management attributed the growth to an AI-first strategy and ongoing product modernization, along with strategic new client agreements and regional adoption in the United States, Mexico, Japan, and India.

Which segments accounted for the revenue growth?

The products business led with Rs 2,936 crore in revenue, up 75% YoY, while services revenue rose to Rs 189 crore, up 6% YoY.

What notable client agreements were announced in the quarter?

Agreements included a major U.S.-vacation ownership company for Lending and Leasing Cloud Service; a Mexican company implementing Oracle Financial Services Analytical Applications; a U.S.-based company increasing its licensed account volume; a Japanese bank adopting Oracle Accounting Foundation and Oracle Financial Services Analytical Applications Cloud Service; a U.S.-headquartered bank signing for Oracle FLEXCUBE Banking; and an Indian bank expanding investments in Oracle Banking and Oracle Financial Services solutions.

When did the quarter end?

The quarter ended June 30, 2026.

What does this mean for OFSS share price in the near term?

The results are described as historic by management, with AI-first strategy and product modernization driving growth; investors may reassess the growth trajectory and the sustainability of earnings expansion, which could influence the ofss share price.

Conclusion

The quarter ending June 30, 2026 shows Oracle Financial Services Software not just delivering strong numbers but also validating a strategic shift toward AI-first product modernization. For retail investors, the implication is double-edged: the growth narrative looks durable, but the stock’s price dynamics will depend on how investors price in sustainability of earnings, competitive positioning, and the pace of client acquisition across global markets. The prudent step is to align expectations with the company’s growth stabilization and to monitor the continuation of sizable deals and product-led revenue momentum.

Open your trading and demat account here

Reference :

1 : Economictimes

Lohia Corp IPO: Should You Apply, Avoid, or Wait for the Listing Dip?

Key Takeaways

- Lohia Corp Limited's OFS-only IPO is priced at ₹404-₹425 with 2,59,31,407 shares aggregating up to ₹1,101 crore and a lot size of 35 shares.

- GMP stands at ₹36 (8.47%) as a live signal, suggesting a potential listing upside, though it's not a guarantee.

- The issue is OFS only with no confirmed Fresh Issue; Registrar and Lead Manager details are To be announced per the data.

- Retail subscription data is not available yet; analyze the price band and OFS structure carefully, as it affects retail allocations and listing dynamics.

Lohia Corp Limited IPO Background: What Does The Company Do And Who Runs It?

The data available confirms only the listing structure: Lohia Corp Limited is launching a main-board OFS-only IPO of 2,59,31,407 equity shares with a face value of ₹1 aggregating up to ₹1,101 crore. The dataset does not provide details about what the company actually does or who the promoters are. The business description, promoters’ background, and market segments will be clarified in the RHP and company filings. Investors should treat this section as incomplete from the provided data and refer to the official RHP for background before forming a view.

IPO Details: Price Band, Lot Size, Issue Size, Dates, Listing Exchanges

Key details according to the source:

- Price Band: ₹404 to ₹425

- Lot Size: 35 shares

- Open Date: 23 Jul 2026

- Close Date: 27 Jul 2026

- Listing Date: 30 Jul 2026

- Exchange: BSE, NSE

- Issue Type: Bookbuilding IPO

- Sale Type: OFS only

- Fresh Issue: To be announced

- OFS: 2,59,31,407 shares of ₹1 (agg. up to ₹1,101cr)

- GMP: ₹36 (8.47%)

- QIB Quota: At least 75% of the Net Offer

- NII Quota: Not more than 15% of the Net Offer

- Retail Quota: Not more than 10% of the Net Offer

- Retail Subscription: Not available yet

- Registrar: To be announced

- Lead Manager: To be announced

- Market Cap: ₹4,490.13 Cr

- Minimum Investment: To be announced

- Face Value: ₹1 per share

Notes: The issuer is an OFS-only offer, with no fresh issue disclosed in the available material. The registrar and lead manager details are listed as To be announced in the data, while the source also mentions MUFG Intime India Pvt.Ltd. as the registrar. Subscriptions for Retail are currently not available in the material.

Lohia Corp IPO GMP Signals And Early Demand View

GMP of ₹36 (8.47%) indicates a potential listing premium based on current demand, which can be interpreted as a positive signal for post-listing performance. However, GMP is a moving indicator and can swing with market appetite, bid pricing, and overall IPO demand. With Retail subscription data not yet available, there is uncertainty about the retail allocation and the final mix of bids. Investors should treat the GMP signal as one of several inputs rather than a guarantee of listing gains.

Lohia Corp Limited IPO Financial Snapshot

| Period | Revenue (₹ Cr) | PAT (₹ Cr) | Borrowings (₹ Cr) |

|---|---|---|---|

| 31 Mar 2026 | ₹1,737.87 | ₹193.45 | ₹152.78 |

| 31 Mar 2025 | ₹1,386.47 | ₹117.84 | ₹212.16 |

Revenue YoY growth: +25.3%

PAT YoY growth: +64.2%

Lohia Corp IPO Valuation, Risk And Who Should Consider This IPO

The price band at ₹404-₹425 implies a market cap of about ₹4,490 crore at the top end, based on the data. The OFS structure means funds are being raised from existing holders rather than new capital for growth, and the absence of a confirmed Fresh Issue adds to execution risk. Retail participation is constrained by a capped 10% of the net offer, with QIBs and NIIs set at higher quotas, which can influence demand dynamics and listing performance. Without a detailed business description in the provided material, investors should be cautious about valuation sufficiency and rely on the official RHP for a complete business and promoter background before committing.

Allotment Odds, Listing Timeline And How To Apply

Open: 23 Jul 2026; Close: 27 Jul 2026; Listing: 30 Jul 2026. Allotment results and final subscription mix will be announced by the exchange and the registrar after bid closure. As of the data, Retail subscription data is not available yet; thus, exact allotment odds for retail investors cannot be computed. To participate, use your broker’s IPO application channel and be mindful of the lot size (35 shares) and the price band (₹404-₹425).

How To Apply For Lohia Corp IPO Via UPI/ASBA

Since this is an OFS and a bookbuilt issue, you can apply through your broker's platform using ASBA, with payment blocked on your bank account linked to your UPI. Steps include: (1) Decide your bidding quantity (one lot is 35 shares, but always confirm via your broker); (2) Log in to your broker's IPO application portal; (3) Enter bid price within the ₹404-₹425 band or as directed; (4) Use ASBA to authorize funds to be blocked by your bank via UPI; (5) Confirm bid and monitor bid status; (6) After allotment results, check your demat and funds; (7) If allotted, ensure shares are in your Demat account post-listing. For tailored, data-driven guidance during the process, consult Swastika's Sarthi AI stock assistant and your Swastika Investmart advisor.

Frequently Asked Questions

Is Lohia Corp IPO worth applying for at ₹404-₹425?

Whether to apply depends on your risk tolerance. The OFS-only structure means funds go to existing shareholders rather than the company, and no confirmed Fresh Issue is disclosed. The GMP of ₹36 suggests potential listing upside, but there is no guarantee post-listing performance. If you can bear listing volatility and you have spare capital, you may consider applying; otherwise, wait for listing day to see demand and price action.

What does the GMP signal mean for listing gains for Lohia Corp IPO?

The GMP of ₹36 indicates a potential listing premium (about 8.47% today) but GMP is only a signal and can move with market demand. It does not guarantee the final listing price or post-listing performance.

What are the main risks of Lohia Corp IPO?

Key risks include the OFS-only structure with no confirmed Fresh Issue, lack of published Retail subscription data, and potential valuation risk given the price band and market conditions. Also, the registrar and lead manager details are listed as To be announced, which could affect processing timelines.

What are the allotment odds for retail investors in the Lohia Corp IPO?

Retail subscription data is not available yet in the provided material, and the net offer allocation caps for Retail are stated as not more than 10% of the Net Offer. Exact allotment odds will depend on the final demand mix once the issue closes.

How do I apply for the Lohia Corp IPO via UPI/ASBA?

To apply via UPI/ASBA, use your broker’s IPO application channel and link your bid to your bank using ASBA. You authorize the bank to block funds for your bid amount through your UPI-linked account, submit the bid within the ₹404-₹425 band, and await allotment results. After allotment, check demat credit and refunds through the allotted broker.

Conclusion

At ₹404-₹425, the Lohia Corp IPO offers an OFS-driven route into a mid-cap universe with a sizeable ₹1,101 crore offering and a live GMP signal suggesting potential listing upside. However, the absence of a confirmed Fresh Issue, the lack of retail subscription data, and the OFS-only structure raise important execution and valuation questions for retail investors. This is a banner that belongs in a watchlist for most small investors who want to see demand confirm itself on listing day before committing capital. If you have high risk tolerance and capital to deploy after observing demand, you could consider applying; otherwise, monitor the listing day to form a data-driven view.

Watchlist – wait for the listing day to confirm demand and price action, and decide with data.

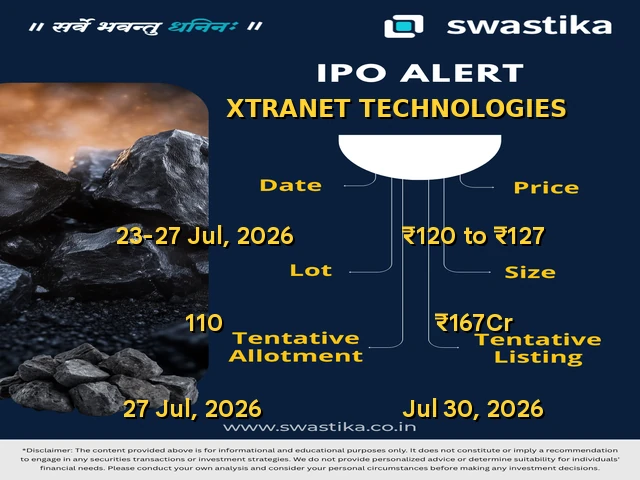

Xtranet Technologies IPO: Should You Apply, Wait, or Skip for Listing Gains?

Key Takeaways

- Xtranet Technologies IPO opens 23–27 Jul 2026; price band ₹120–₹127; 1,31,34,000 fresh shares aggregating ₹167 Cr.

- GMP data is not available yet; no listing gain signal.

- Market cap around ₹664.03 Cr; FY2026 Revenue ₹366.01 Cr; PAT ₹40.73 Cr; Revenue YoY growth +32.4%; PAT YoY growth +35.6%.

- Action: watchlist for now; wait for GMP signals and registrar/lead-manager clarity before applying.

Xtranet Technologies IPO Details

- Price band: ₹120 to ₹127

- Lot size: 110 Shares

- Issue size: 1,31,34,000 shares (agg. up to ₹167 Cr)

- Min Investment: To be announced

- Face Value: ₹10 per share

- Exchange: BSE, NSE

- Issue Type: Bookbuilding IPO

- Sale Type: Fresh capital only

- Fresh Issue: 1,31,34,000 shares (agg up to ₹167 Cr)

- OFS: To be announced

- GMP: Not available yet

- QIB Quota: 39,40,200

- NII Quota: To be announced

- Retail Quota: To be announced

- Registrar: To be announced

- Lead Manager: To be announced

- Market Cap: ₹664.03 Cr

Xtranet Technologies IPO Background And Business Overview

The available material identifies Xtranet Technologies Limited as a main-board IPO with a fresh issue of 1,31,34,000 shares aggregating ₹167 Cr, priced in the band ₹120 to ₹127. The document does not provide promoter names or a detailed business description in the provided material. Registrar and lead managers are labeled as To be announced. The shares are proposed to be listed on BSE and NSE.

Xtranet Technologies IPO Financial Highlights

| Period | Revenue | PAT | Net Worth | Borrowings |

|---|---|---|---|---|

| 31 Mar 2026 | ₹366.01 Cr | ₹40.73 Cr | ₹136.01 Cr | ₹85.45 Cr |

| 31 Mar 2025 | ₹276.53 Cr | ₹30.03 Cr | ₹95.49 Cr | ₹39.24 Cr |

Revenue YoY growth: +32.4%; PAT YoY growth: +35.6%

Xtranet Technologies IPO Valuation: Is The ₹120–₹127 Band Fair?

Based on the numbers provided, the market cap is ₹664.03 Cr. With FY2026 PAT of ₹40.73 Cr, the rough P/E sits around 16.3x (664.03 ÷ 40.73). Revenue growth in FY2026 was +32.4% YoY, and PAT grew +35.6%, suggesting momentum, but the data is limited to two years and there is no additional guidance on margins or sustainability. The absence of promoter details, details about the registrar/lead managers, and the lack of live GMP data mean the listing could swing either way. Investors should treat this as a mid-cap growth story with execution risk until more details emerge. For deeper analysis, you can use Swastika's Sarthi AI stock assistant.

Key Risks To Consider In Xtranet Technologies IPO

- Promoter and business details are not disclosed in the provided material, limiting visibility into the underlying business risk.

- Registrar and Lead Manager are to be announced, creating execution and processing risk.

- GMP data is not available yet, so listing gain expectations are unclear.

- Retail and other quota details are not disclosed yet, making bid strategy uncertain.

- Fresh issue structure means the capital is being raised pre-listing; the post-IPO company structure depends on the fledgling market reception.

Allotment &Amp Listing Timeline

The IPO opens on 23 July 2026 and closes on 27 July 2026. The listing is expected on 30 July 2026 on BSE and NSE.

Frequently Asked Questions

Is Xtranet Technologies IPO worth applying for at ₹120–₹127?

The decision depends on your risk tolerance and appetite for uncertainty. The company shows two years of revenue and PAT growth, but GMP data is not available yet, and key details like registrar/lead-manager are not announced. Consider waiting for more clarity and the actual listing performance before committing.

What does GMP status mean for this IPO?

GMP data for Xtranet Technologies IPO is not available yet, so there is no listing gain signal to guide bidding or pricing expectations at this time.

What is the lot size and minimum investment for this IPO?

Lot size is 110 shares. The minimum investment amount is not announced yet.

When will the registrar and lead manager be announced?

Registrar and lead managers are to be announced. Until then, bid support and after-market processes remain uncertain.

When is the listing date and how should I approach applying?

The listing date is 30 July 2026. Open 23 July and close 27 July 2026. Given the current lack of GMP data and incomplete bid details, consider waiting for more clarity or applying only if you have a high risk tolerance and a post-listing plan.

Conclusion

Xtranet Technologies IPO presents a mid-cap growth opportunity with a modest ₹167 Cr fresh issue and a price band of ₹120–₹127, supported by two years of solid revenue and PAT growth. However, key details are missing – promoter background, registrar/lead-manager information, and live GMP signals – creating uncertainty about the listing performance. This is a classic “watchlist” scenario for most retail investors who want clarity before committing capital.

Investors should align this with their risk tolerance and post-listing plans. A cautious approach would be to observe the listing day and decide with data; watch the GMP signal and the final allotment details before acting.

.jpg)

Xtranet Technologies IPO Review: Should You Subscribe? GMP, Financials, Risks & Analysis

Executive Summary

Xtranet Technologies is entering the primary market with a ₹166.80 crore fresh issue, aiming to strengthen its balance sheet and fund future business growth. Unlike many IPOs where promoters are partially exiting, this issue channels the proceeds directly into the business through working capital support, debt reduction, and infrastructure expansion.

From an investment perspective, the company presents a mixed but interesting opportunity. On one hand, it has delivered consistent revenue and profit growth, maintains a healthy order book, serves several marquee government and enterprise clients, and is available at a valuation that appears lower than many listed IT peers. On the other hand, investors should carefully evaluate its dependence on government contracts, concentration of revenue among a handful of customers, long receivable cycles, and ongoing litigation before making an investment decision.

For investors looking beyond short-term listing gains, the IPO offers exposure to India's growing enterprise digital transformation market at a relatively reasonable valuation. However, the business will need to demonstrate that it can diversify its customer base, improve working capital efficiency, and sustain earnings growth after listing.

Try Sarthi - Your AI Stock Assistant

Xtranet Technologies IPO Snapshot

Why Investors are Interested in Xtranet Technologies IPO?

Every IPO has a story, but not every story translates into a quality investment. Xtranet Technologies is attracting attention because it operates in one of India's fastest-growing industries—enterprise IT services and digital transformation. Businesses, government departments, and public sector organisations continue to increase spending on cloud infrastructure, cybersecurity, automation, analytics, and enterprise software. This structural trend provides long-term opportunities for companies capable of delivering integrated technology solutions.

What makes Xtranet different is that it does not operate solely as a software developer. Instead, it combines consulting, implementation, infrastructure integration, managed services, cybersecurity, and proprietary software platforms into a comprehensive technology offering. This integrated approach enables the company to work on large digital transformation projects rather than isolated software assignments.

Another factor supporting investor interest is the issue's valuation. At the upper price band, Xtranet is offered at a P/E ratio of 12.21x, considerably lower than several listed IT service companies. While valuation alone does not determine investment quality, it provides investors with a relatively comfortable entry point if the company continues delivering consistent growth.

Xtranet Technologies' Business - A Key Overview

Founded in 2002, Xtranet Technologies has spent more than two decades building expertise in enterprise IT solutions. Over the years, the company has expanded from traditional IT implementation services into a broader digital transformation partner for government organisations, PSUs, and private enterprises.

Today, its operations span multiple technology verticals, including:

- Enterprise Application Development

- Cloud & Infrastructure Services

- Cybersecurity

- Enterprise Resource Planning (ERP)

- Intelligent Automation

- Data Analytics

- Managed IT Services

- Digital Transformation Consulting

Instead of offering a single product, the company works closely with clients to design, deploy, integrate, and maintain complete technology ecosystems. This creates opportunities for recurring business through maintenance contracts, managed services, software upgrades, and long-term technology partnerships.

The company has also invested in building proprietary technology platforms, reducing its dependence on third-party software while strengthening customer stickiness. Some of its key platforms include:

- Synergy, a low-code digital transformation platform

- X-ERP, designed for enterprise resource planning

- XtraTrust, focused on secure digital authentication

- NeuraFlow, an intelligent workflow automation platform

These solutions not only expand the company's service portfolio but also help improve margins through higher-value software offerings.

Client Base of Xtranet Technologies

One of Xtranet Technologies' strongest competitive advantages is the quality of its customer portfolio. Winning projects from government organisations and large enterprises requires strict compliance, technical expertise, and execution capability. Over the years, the company has built relationships with several well-known organisations, including:

- BSNL

- Indian Oil Corporation

- RailTel

- Food Corporation of India (FCI)

- Delhi Police

- Mumbai Metro

- Income Tax Department

These projects often involve large-scale digital transformation initiatives where reliability and execution become more important than simply offering the lowest price.

The company's capabilities were further demonstrated in March 2026, when it participated in a consortium that secured a ₹108.77 crore contract to modernise banking systems in Haryana.

Such projects strengthen Xtranet's credentials and can improve its ability to compete for future government and enterprise contracts.

Industry Tailwinds Continue to Support Growth

The long-term demand outlook for enterprise technology services remains favourable. Across both public and private sectors, organisations are investing in:

- Cloud migration

- Enterprise cybersecurity

- Artificial intelligence

- Data analytics

- Intelligent automation

- Digital governance

- Workflow digitisation

- ERP modernisation

Government initiatives aimed at improving digital public infrastructure and expanding e-governance are creating additional opportunities for IT solution providers. At the same time, enterprises are increasingly replacing legacy systems with integrated cloud-based platforms to improve operational efficiency and customer experience.

These trends create a supportive environment for companies like Xtranet Technologies that provide end-to-end technology solutions. However, industry growth alone does not guarantee business success. Companies must continue winning new contracts, executing projects efficiently, and maintaining profitability to benefit from these long-term trends.

Growth Drivers that Could Support Future Performance of Xtranet Technologies

Several factors could contribute to Xtranet Technologies' growth over the coming years.

Healthy Order Book

As of April 30, 2026, the company reported an unexecuted order book of ₹356.96 crore. This provides meaningful revenue visibility and indicates that a significant portion of future business has already been secured.

Expansion of Proprietary Platforms

By investing in internally developed platforms such as Synergy and XtraTrust, the company aims to strengthen recurring revenue while differentiating itself from traditional IT service providers.

Increasing Enterprise Digitalisation

Growing investments in automation, cybersecurity, ERP implementation, and cloud services are expanding the addressable market for enterprise technology companies.

Infrastructure Expansion

The company holds a 99-year lease from the Government of Madhya Pradesh for land dedicated to IT Park operations. This provides flexibility for future expansion as business requirements evolve.

Fresh Capital Through the IPO

Unlike an Offer for Sale, this IPO will inject capital directly into the company. Improved liquidity and lower debt could support faster project execution and stronger financial flexibility over the medium term.

Not Every Growth Story is Risk-Free

While the company's growth prospects appear encouraging, investors should avoid viewing the IPO only through the lens of revenue and profit growth.

Some of the strongest concerns surrounding Xtranet Technologies relate to customer concentration, receivable management, government dependency, and litigation. These issues do not necessarily make the IPO unattractive, but they require careful evaluation because they can influence future earnings and cash flows.

A balanced investment decision should weigh these risks against the company's attractive valuation, improving profitability, and expanding business opportunities.

Financial Performance of Xtranet Technologies: Growth Backed by Improving Profitability

One of the strongest positives for Xtranet Technologies is that its earnings growth has remained consistent over the last few financial years. The company has not only increased its revenue but has also improved profitability, indicating better operational efficiency.

Financial Snapshot (FY26)

A notable takeaway is that profit has grown faster than revenue, suggesting the company has been able to improve execution and control costs while expanding its operations.

The EBITDA margin has also strengthened significantly compared to earlier years, reflecting improved operational efficiency. For investors, this is an encouraging sign because sustainable profit growth generally creates more value than revenue growth alone.

A Strong Order Book Supports Future Revenue

For project-based IT companies, the order book often provides a clearer picture of future business than past financial performance. As of April 30, 2026, Xtranet Technologies reported an unexecuted order book of ₹356.96 crore.

Considering that the company generated total income of ₹366.01 crore during FY26, this order pipeline represents a substantial amount of future business already secured. A healthy order book offers several advantages:

- Better revenue visibility

- Improved business stability

- Higher confidence in future earnings

- Reduced dependence on winning new contracts every quarter

However, investors should remember that order books translate into revenue only when projects are executed successfully and payments are received on time.

The IPO Structure is a Fresh Issue?

One aspect that differentiates Xtranet Technologies from many recent IPOs is its 100% fresh issue structure. Unlike an Offer for Sale (OFS), where existing shareholders sell their shares and retain the proceeds, a fresh issue brings new capital directly into the company.

This is generally viewed positively because the funds are used to strengthen the business rather than facilitate promoter exits.

Planned Use of IPO Proceeds

The largest allocation is towards working capital, reflecting the nature of enterprise IT projects, which often require significant upfront investments before payments are received.

Reducing debt should also improve the company's financial flexibility, while capital expenditure on hardware and IT infrastructure is expected to support future project execution.

Competitive Position: More Than a Traditional IT Services Company

Xtranet Technologies competes in the broader IT services and digital transformation industry, but its business model goes beyond conventional software development.

The company combines consulting, software implementation, infrastructure integration, cybersecurity, managed services, and proprietary software products under one umbrella.

This integrated approach allows it to participate in large digital transformation projects where clients prefer a single technology partner instead of managing multiple vendors.

Its competitive positioning is further supported by:

- Proprietary Platforms: Synergy, X-ERP, XtraTrust, and NeuraFlow.

- Industry Certifications: CMMI-SVC-ML-5, ISO 9001, ISO 27001, and ISO 20000.

- Government Experience: Execution of complex projects for PSUs and government departments.

- Long-Term Client Relationships: Repeat business from enterprise and public sector clients.

- Specialised Infrastructure: Dedicated innovation labs focusing on technologies such as RFID and GPS tracking.

While the company is smaller than many listed IT peers, these capabilities help differentiate it in niche enterprise and government technology projects.

Is the Xtranet Technologies IPO Fairly Valued?

Valuation plays an important role in determining whether an IPO offers sufficient upside relative to its risks. At the upper price band of ₹127, Xtranet Technologies is valued at a pre-IPO Price-to-Earnings (P/E) ratio of 12.21x.

When compared with listed peers, the valuation appears relatively conservative.

Although direct comparisons should be made cautiously due to differences in scale, service offerings, and client mix, the lower valuation provides a degree of comfort for investors.

The company also reports stronger return ratios than many businesses listed at significantly higher earnings multiples. From a valuation perspective, the IPO appears reasonably priced rather than aggressively valued.

Risk Assessment: What Investors Should Watch Closely?

Every investment opportunity comes with risks, and understanding them is just as important as evaluating the positives.

Customer Concentration

The company derives 86.72% of FY26 revenue from its top ten customers, while the single largest customer contributes over 23%.

Such concentration creates dependence on a limited number of relationships. Losing a major customer or experiencing delays in large contracts could have a noticeable impact on revenue and profitability.

Diversifying the customer base will be an important long-term objective for the company.

Dependence on Government and PSU Contracts

Approximately 47% of FY26 revenue comes from government departments and public sector undertakings. Government projects generally provide credibility and large contract values, but they also involve:

- Competitive tendering

- Administrative approvals

- Budget constraints

- Delayed payments

- Longer execution timelines

Any slowdown in government spending or unsuccessful bids could affect future growth.

Working Capital Remains a Challenge

Enterprise technology projects typically involve extended payment cycles, and Xtranet is no exception. The company often provides customers with credit periods ranging from 150 to 210 days.

As a result:

- Trade receivables remain high.

- Additional working capital is required.

- Borrowings may increase during periods of rapid expansion.

The allocation of IPO proceeds toward working capital should help improve liquidity, but investors should continue monitoring receivable management after listing.

Rising Debt Levels

Despite strong earnings growth, the company's debt profile has also expanded. Net debt increased from ₹38.32 crore in FY25 to ₹84.15 crore in FY26, while the Debt-to-Equity ratio rose to 0.63x.

In addition, the Debt Service Coverage Ratio (DSCR) declined from 3.43x to 2.35x, indicating a lower cushion for servicing debt. The planned repayment of borrowings through IPO proceeds is therefore an important positive for the company's balance sheet.

Significant Litigation

One of the most closely watched issues is the ongoing legal dispute involving Hitachi Systems India. Xtranet Technologies is seeking recovery of ₹58.57 crore, including interest.

The amount involved exceeds the company's FY26 net profit, making the case financially material. The statutory auditor has also highlighted the matter in the audit report, noting that a corresponding interest liability has not yet been recognised pending the court's final decision. Although the final outcome remains uncertain, investors should monitor future developments carefully.

Vendor Concentration

The company's hardware integration business depends heavily on external suppliers. Its top ten suppliers accounted for more than 95% of total purchases in FY26. Any disruption in supply chains, changes in pricing, or issues with key vendors could affect project execution and margins.

Geographic Concentration

Despite serving clients across India, approximately 85.72% of FY26 revenue originated from only three regions:

- Maharashtra

- Madhya Pradesh

- Delhi

Expanding into additional states and private-sector markets could reduce this concentration risk over time.

What Does the Grey Market Premium (GMP) Suggest?

As of July 22, 2026, the Xtranet Technologies IPO GMP is reported in the range of ₹20 to ₹23 per share. Based on the upper price band of ₹127, this indicates an estimated listing price of around ₹147 to ₹150, implying a potential listing gain of approximately 16% to 18%, if current sentiment remains unchanged.

The GMP has fluctuated between ₹18 and ₹26 over the past week, reflecting healthy investor interest while also showing that market expectations continue to evolve. It's important to remember that the Grey Market Premium is an unofficial indicator based on market sentiment. It should not be considered a guarantee of listing performance or the sole reason to invest in an IPO.

Who Should Consider Investing in Xtranet Technologies?

Like most IPOs, Xtranet Technologies may not be suitable for every investor.

Suitable for Investors Who:

- Prefer investing in growing IT and digital transformation businesses.

- Have a medium to long-term investment horizon.

- Appreciate reasonably valued companies with improving profitability.

- Are comfortable with moderate business and execution risks.

- Want exposure to India's enterprise technology and government digitalisation initiatives.

Investors Who May Prefer to Wait

The IPO may be less suitable for investors who:

- Prefer businesses with highly diversified customer bases.

- Are uncomfortable with long receivable cycles and working capital-intensive operations.

- Prefer companies with lower dependence on government contracts.

- Seek businesses with minimal litigation and stronger cash flow history.

Understanding your own risk appetite is as important as evaluating the company's fundamentals before making any IPO investment.

Investor Checklist About Xtranet Technologies' IPO

Before applying for the IPO, consider the following factors:

Positives

- Fresh issue, with proceeds supporting business growth.

- Revenue increased by 32% in FY26.

- Profit after tax grew by 36%.

- Healthy ROE of 34.78% and ROCE of 32.52%.

- Strong order book of ₹356.96 crore.

- Exposure to India's expanding digital transformation market.

- Proprietary software platforms and enterprise solutions.

- Reasonable valuation compared with listed peers.

Risks

- High dependence on the top 10 customers.

- Nearly half of revenue comes from government and PSU contracts.

- Long receivable cycle affecting working capital.

- Rising debt before the IPO.

- Ongoing litigation with Hitachi Systems India.

- Geographic concentration in three major regions.

Reviewing both the positives and risks can help investors make a more balanced decision instead of relying solely on market sentiment or GMP.

Frequently Asked Questions (FAQs)

Is Xtranet Technologies' IPO a fresh issue or an Offer for Sale?

The IPO is a 100% fresh issue, meaning the funds raised will go directly to the company for business expansion, working capital, debt repayment, and general corporate purposes.

Why is working capital a major focus for Xtranet Technologies?

The company executes large enterprise and government projects where payments are often received several months after project execution. This creates higher working capital requirements, making additional funding important for future growth.

What makes Xtranet Technologies different from traditional IT service companies?

Apart from IT implementation and managed services, the company has developed proprietary platforms such as Synergy, X-ERP, XtraTrust, and NeuraFlow, allowing it to offer integrated digital transformation solutions instead of only manpower-based services.

How important is the current order book?

The company's unexecuted order book of ₹356.96 crore provides visibility into future revenue. However, revenue recognition depends on successful project execution and timely customer payments.

Why do analysts mention customer concentration as a risk?

A significant portion of the company's revenue comes from a limited number of customers. If any major client reduces spending or delays projects, it could affect revenue and profitability.

Does the IPO help reduce debt?

Yes. A portion of the IPO proceeds is allocated toward repaying borrowings, which may improve the company's balance sheet and reduce future interest costs.

What is the significance of the Hitachi Systems India litigation?

The legal dispute involves a claim of ₹58.57 crore, which is larger than the company's FY26 net profit. While the outcome remains uncertain, investors should monitor future developments as they may have financial implications.

Final Verdict: Should You Subscribe to the Xtranet Technologies IPO?

Xtranet Technologies enters the market with steady financial growth, a healthy order book, and exposure to India's expanding digital transformation sector. While its long-term prospects appear promising, investors should carefully evaluate the associated business risks and valuation before making an investment decision. For more IPO reviews, stock market updates, and expert market insights, follow the latest research and analysis from Swastika Investmart.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App