From Inflation to Bond Yields: Understanding Interest Rate Cycles & Market Impact.

Key Takeaways

- Inflation directly influences interest rate decisions by central banks

- Rising inflation pushes bond yields higher and impacts equity valuations

- Interest rate cycles affect different sectors in different ways

- Bond markets react faster than equities to macro changes

- Smart asset allocation helps investors navigate these cycles

Introduction

If you have ever wondered why markets suddenly turn volatile or why borrowing costs change, the answer often lies in three interconnected factors: inflation, bond yields, and interest rate cycles.

At the center of this ecosystem is the Reserve Bank of India, which adjusts policy rates to balance growth and inflation. These decisions ripple through bond markets, equity markets, and ultimately your investment portfolio.

Understanding this chain reaction is essential for investors who want to stay ahead rather than react late.

What is Inflation and Why It Matters

Inflation refers to the rise in prices of goods and services over time. While moderate inflation is a sign of healthy demand, excessive inflation can disrupt economic stability.

Real-World Example

When fuel prices increase, transportation costs go up. This affects everything from groceries to manufacturing. As a result, consumers end up paying more across categories.

👉 This is how inflation spreads across the economy

How Inflation Impacts Interest Rates

Central banks use interest rates as a tool to control inflation.

When Inflation Rises

- Central bank increases interest rates

- Borrowing becomes expensive

- Demand slows down

When Inflation Falls

- Central bank cuts interest rates

- Borrowing becomes cheaper

- Consumption and investment rise

The Policy Role

The Reserve Bank of India closely tracks inflation trends before making policy decisions. Its primary goal is to maintain price stability while supporting growth.

Understanding Interest Rate Cycles

Interest rate cycles move in phases depending on economic conditions.

📉 Easing Phase

- Rates are reduced

- Liquidity increases

- Equity markets tend to perform well

📈 Tightening Phase

- Rates are increased

- Liquidity tightens

- Market valuations may compress

⏸️ Pause Phase

- Rates remain unchanged

- Markets turn data-dependent

- Volatility can remain high

Bond Yields: The Missing Link

Bond yields are often the first indicators of changing economic conditions.

What Are Bond Yields?

Bond yield is the return an investor earns on a bond.

Relationship Between Inflation and Bond Yields

- Rising inflation leads to higher bond yields

- Falling inflation leads to lower bond yields

👉 Key Rule:

When yields rise, bond prices fall, and vice versa

Why Bond Markets React First

Bond investors closely monitor:

- Inflation data

- Interest rate expectations

- Fiscal policies

👉 This makes bond markets more sensitive and quicker to react than equity markets

Impact on Equity Markets

Equity markets respond differently depending on the stage of the cycle.

🔴 High Inflation and Rising Rates

- Valuations come under pressure

- Growth stocks may correct

- Cost-sensitive sectors struggle

🟢 Stable Inflation and Lower Rates

- Earnings visibility improves

- Liquidity supports valuations

- Market sentiment turns positive

Sector-Wise Impact in India

🚀 Beneficiaries

- Banking sector during rising rates

- Commodities and energy during inflation spikes

⚠️ Challenged Sectors

- Real estate and auto due to higher borrowing costs

- FMCG due to input cost pressures

Practical Example from Indian Markets

During periods of rising inflation in India, bond yields have historically moved higher, leading to cautious equity market behavior. Rate-sensitive sectors such as real estate and auto often underperform, while banks may benefit from improved margins.

This pattern reinforces the importance of tracking macro indicators rather than focusing only on stock-specific news.

How Investors Should Respond

Understanding macro cycles can significantly improve investment decisions.

🧠 1. Focus on Asset Allocation

Balance between equity, debt, and other assets

📊 2. Track Bond Yields

They often signal upcoming changes in interest rates

📉 3. Adjust Sector Exposure

Reduce exposure to rate-sensitive sectors during tightening phases

⏳ 4. Stay Long-Term Focused

Short-term volatility is part of market cycles

Why This Matters More Today

With global uncertainties, commodity price fluctuations, and changing inflation trends, interest rate cycles have become more dynamic.

For Indian investors, this means:

- More frequent market shifts

- Greater importance of macro awareness

- Need for disciplined investing

FAQs

1. What is the relationship between inflation and bond yields?

Rising inflation usually leads to higher bond yields, while falling inflation leads to lower yields.

2. How do interest rate cycles affect stock markets?

Rate hikes can pressure valuations, while rate cuts generally support market growth.

3. Why do bond markets react faster than equity markets?

Bond markets are more sensitive to macroeconomic changes like inflation and interest rates.

4. Which sectors perform well during rising interest rates?

Banking and financial sectors may benefit, while rate-sensitive sectors may struggle.

5. How should investors use this information?

Investors should track macro indicators, diversify their portfolios, and adjust strategies based on economic cycles.

Conclusion

From inflation to bond yields and interest rate cycles, the connection is clear. These factors shape market direction and influence investment outcomes more than short-term news flows.

For investors, the goal is not to predict every move but to understand the cycle and position accordingly.

At Swastika Investmart, we combine deep market research, advanced tools, and investor education to help you navigate complex market environments with confidence.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

From Inflation to Bond Yields: Understanding Interest Rate Cycles & Market Impact.

Key Takeaways

- Inflation directly influences interest rate decisions by central banks

- Rising inflation pushes bond yields higher and impacts equity valuations

- Interest rate cycles affect different sectors in different ways

- Bond markets react faster than equities to macro changes

- Smart asset allocation helps investors navigate these cycles

Introduction

If you have ever wondered why markets suddenly turn volatile or why borrowing costs change, the answer often lies in three interconnected factors: inflation, bond yields, and interest rate cycles.

At the center of this ecosystem is the Reserve Bank of India, which adjusts policy rates to balance growth and inflation. These decisions ripple through bond markets, equity markets, and ultimately your investment portfolio.

Understanding this chain reaction is essential for investors who want to stay ahead rather than react late.

What is Inflation and Why It Matters

Inflation refers to the rise in prices of goods and services over time. While moderate inflation is a sign of healthy demand, excessive inflation can disrupt economic stability.

Real-World Example

When fuel prices increase, transportation costs go up. This affects everything from groceries to manufacturing. As a result, consumers end up paying more across categories.

👉 This is how inflation spreads across the economy

How Inflation Impacts Interest Rates

Central banks use interest rates as a tool to control inflation.

When Inflation Rises

- Central bank increases interest rates

- Borrowing becomes expensive

- Demand slows down

When Inflation Falls

- Central bank cuts interest rates

- Borrowing becomes cheaper

- Consumption and investment rise

The Policy Role

The Reserve Bank of India closely tracks inflation trends before making policy decisions. Its primary goal is to maintain price stability while supporting growth.

Understanding Interest Rate Cycles

Interest rate cycles move in phases depending on economic conditions.

📉 Easing Phase

- Rates are reduced

- Liquidity increases

- Equity markets tend to perform well

📈 Tightening Phase

- Rates are increased

- Liquidity tightens

- Market valuations may compress

⏸️ Pause Phase

- Rates remain unchanged

- Markets turn data-dependent

- Volatility can remain high

Bond Yields: The Missing Link

Bond yields are often the first indicators of changing economic conditions.

What Are Bond Yields?

Bond yield is the return an investor earns on a bond.

Relationship Between Inflation and Bond Yields

- Rising inflation leads to higher bond yields

- Falling inflation leads to lower bond yields

👉 Key Rule:

When yields rise, bond prices fall, and vice versa

Why Bond Markets React First

Bond investors closely monitor:

- Inflation data

- Interest rate expectations

- Fiscal policies

👉 This makes bond markets more sensitive and quicker to react than equity markets

Impact on Equity Markets

Equity markets respond differently depending on the stage of the cycle.

🔴 High Inflation and Rising Rates

- Valuations come under pressure

- Growth stocks may correct

- Cost-sensitive sectors struggle

🟢 Stable Inflation and Lower Rates

- Earnings visibility improves

- Liquidity supports valuations

- Market sentiment turns positive

Sector-Wise Impact in India

🚀 Beneficiaries

- Banking sector during rising rates

- Commodities and energy during inflation spikes

⚠️ Challenged Sectors

- Real estate and auto due to higher borrowing costs

- FMCG due to input cost pressures

Practical Example from Indian Markets

During periods of rising inflation in India, bond yields have historically moved higher, leading to cautious equity market behavior. Rate-sensitive sectors such as real estate and auto often underperform, while banks may benefit from improved margins.

This pattern reinforces the importance of tracking macro indicators rather than focusing only on stock-specific news.

How Investors Should Respond

Understanding macro cycles can significantly improve investment decisions.

🧠 1. Focus on Asset Allocation

Balance between equity, debt, and other assets

📊 2. Track Bond Yields

They often signal upcoming changes in interest rates

📉 3. Adjust Sector Exposure

Reduce exposure to rate-sensitive sectors during tightening phases

⏳ 4. Stay Long-Term Focused

Short-term volatility is part of market cycles

Why This Matters More Today

With global uncertainties, commodity price fluctuations, and changing inflation trends, interest rate cycles have become more dynamic.

For Indian investors, this means:

- More frequent market shifts

- Greater importance of macro awareness

- Need for disciplined investing

FAQs

1. What is the relationship between inflation and bond yields?

Rising inflation usually leads to higher bond yields, while falling inflation leads to lower yields.

2. How do interest rate cycles affect stock markets?

Rate hikes can pressure valuations, while rate cuts generally support market growth.

3. Why do bond markets react faster than equity markets?

Bond markets are more sensitive to macroeconomic changes like inflation and interest rates.

4. Which sectors perform well during rising interest rates?

Banking and financial sectors may benefit, while rate-sensitive sectors may struggle.

5. How should investors use this information?

Investors should track macro indicators, diversify their portfolios, and adjust strategies based on economic cycles.

Conclusion

From inflation to bond yields and interest rate cycles, the connection is clear. These factors shape market direction and influence investment outcomes more than short-term news flows.

For investors, the goal is not to predict every move but to understand the cycle and position accordingly.

At Swastika Investmart, we combine deep market research, advanced tools, and investor education to help you navigate complex market environments with confidence.

Why Rising Oil Prices and Inflation May Force RBI to Pause Rate Cuts

Key Takeaways

- Rising crude oil prices are pushing inflation risks higher

- Higher inflation limits the ability of RBI to cut interest rates

- Rate pause can impact equity markets and borrowing costs

- Oil-sensitive sectors may face pressure in the short term

- Investors should focus on diversification and quality stocks

Introduction

The global economic environment is once again turning uncertain, with crude oil prices inching higher and inflation concerns resurfacing. For India, this combination creates a challenging situation for policymakers, especially the Reserve Bank of India.

At a time when markets were expecting further rate cuts to support growth, rising inflationary pressures may force the central bank to take a pause. This shift has important implications for investors, borrowers, and the overall market direction.

The Link Between Oil Prices and Inflation

India is heavily dependent on crude oil imports, which makes it highly sensitive to global price movements.

How Rising Oil Prices Impact Inflation

- Higher fuel costs increase transportation expenses

- Logistics costs rise across industries

- Raw material prices move up

- End consumers face higher prices

👉 This leads to cost-push inflation, where rising input costs push overall prices higher

Real-World Context

Whenever crude oil prices spike globally, India often experiences a rise in retail fuel prices. This directly affects household budgets and reduces disposable income, slowing consumption demand.

Why RBI May Pause Rate Cuts

Central banks balance two key objectives:

- Supporting economic growth

- Controlling inflation

When inflation rises, controlling it becomes the priority.

The Policy Dilemma

- Rate cuts help boost growth by making loans cheaper

- But they can also increase inflation by boosting demand

👉 In a high inflation environment, cutting rates becomes risky

Current Scenario

- Rising oil prices are adding inflationary pressure

- Global uncertainties are increasing volatility

- Currency fluctuations can further amplify imported inflation

👉 This leaves the Reserve Bank of India with limited room to ease monetary policy

Impact on Indian Markets

A pause in rate cuts can influence multiple segments of the market.

📊 1. Equity Markets

- Rate-sensitive sectors may underperform

- Valuations may remain under pressure

- Market sentiment could turn cautious

🏦 2. Banking and NBFC Sector

- Loan growth may stabilize rather than accelerate

- Margins could remain steady but not expand significantly

🏠 3. Realty and Auto

- Higher borrowing costs may impact demand

- Consumer financing becomes less attractive

🛢️ 4. Energy Sector

- Upstream companies may benefit from higher oil prices

- Downstream companies may face margin pressure

Bond Market Perspective

Bond markets react quickly to inflation and interest rate expectations.

What Happens When Inflation Rises

- Bond yields tend to move higher

- Bond prices fall

- Long-duration bonds become less attractive

👉 Investors may prefer shorter-duration fixed income instruments during such phases

What Should Investors Do?

Market conditions like these require a balanced and disciplined approach.

🧠 1. Focus on Asset Allocation

Maintain a mix of equity, debt, and other asset classes

📉 2. Avoid Overexposure to Rate-Sensitive Stocks

Sectors like real estate and auto may face short-term pressure

📊 3. Look for Quality Businesses

Companies with:

- Strong pricing power

- Stable demand

- Healthy balance sheets

tend to perform better during inflationary periods

⏳ 4. Stay Invested for the Long Term

Short-term volatility should not derail long-term investment goals

A Broader Perspective

Historically, periods of rising oil prices and inflation have led to cautious monetary policy globally. India is no exception.

For example, during earlier commodity cycles, central banks often paused or delayed rate cuts until inflation showed signs of cooling. This pattern reinforces the importance of monitoring macroeconomic indicators.

Key Indicators to Watch

- Crude oil price trends

- CPI inflation data

- RBI policy statements

- Global economic developments

Tracking these indicators can provide early signals of policy direction.

FAQs

1. Why do rising oil prices impact inflation?

Because oil affects transportation and production costs, which increases the overall price of goods and services.

2. Why might RBI pause rate cuts?

To control inflation and maintain economic stability, especially when price pressures are rising.

3. How does this affect stock markets?

It can lead to cautious sentiment, especially in rate-sensitive sectors, while some sectors like energy may benefit.

4. What happens to bond yields in this scenario?

Bond yields usually rise when inflation increases, leading to a fall in bond prices.

5. What should investors do during such phases?

Maintain diversification, focus on quality investments, and avoid making decisions based on short-term volatility.

Conclusion

Rising oil prices and inflation are key factors shaping the current economic landscape. While markets were hoping for continued rate cuts, the reality is that the Reserve Bank of India may need to stay cautious.

For investors, this is not a time to panic but to adapt. A well-diversified portfolio, combined with a focus on quality and long-term discipline, can help navigate such phases effectively.

At Swastika Investmart, we empower investors with research-driven insights, advanced trading tools, and strong customer support to make informed decisions in changing market conditions.

21 Hours, No Agreement: What’s Next After US-Iran Talks Collapse?

Key Takeaways

- US-Iran talks ended without a deal after 21 hours of negotiations

- Rising tensions may lead to supply risks and higher oil prices

- Global markets could see increased volatility in the near term

- Indian markets may face pressure via inflation and currency movement

- Investors should stay cautious and focus on diversified portfolios

Introduction

After nearly 21 hours of intense negotiations, the much-anticipated US-Iran talks ended without any agreement. The development has once again brought geopolitical tensions into focus, with potential ripple effects across global markets.

Statements from leaders like Donald Trump and JD Vance indicate that the situation could escalate further, with options such as restricting Iran’s oil exports being considered.

For investors, especially in India, this is not just a political headline. It is a macro event that can influence oil prices, inflation, currency, and overall market sentiment.

What Happened in the US-Iran Talks?

The talks, held in Islamabad, were aimed at reaching a breakthrough on key issues, particularly Iran’s nuclear-related commitments. However, despite prolonged discussions, both sides failed to reach common ground.

Key Highlights:

- Negotiations lasted around 21 hours

- The US presented what it called its “final and best offer”

- No agreement was reached on core demands

- Strategic pressure options, including trade and oil restrictions, are being discussed

This outcome signals a shift from diplomacy toward increased geopolitical pressure.

Why This Matters Globally

The US and Iran are critical players in the global energy ecosystem. Any disruption in their relationship can have far-reaching consequences.

1. Oil Supply Risks

Iran is a key oil exporter. Any restriction on its exports can tighten global supply.

👉 Result: Oil prices may rise sharply

2. Inflation Concerns

Higher oil prices directly impact:

- Transportation costs

- Manufacturing expenses

- Consumer prices

This can push global inflation higher, complicating central bank policies.

3. Market Volatility

Geopolitical uncertainty often leads to:

- Equity market corrections

- Flight to safe-haven assets like gold

- Currency fluctuations

Impact on Indian Markets

India, being a major oil importer, is particularly sensitive to such developments.

📊 1. Crude Oil and Inflation

- India imports more than 80 percent of its crude oil needs

- Rising oil prices can increase inflation

👉 This may limit the flexibility of the Reserve Bank of India in cutting interest rates

📉 2. Equity Market Reaction

- Sectors like aviation, paints, and logistics may face cost pressures

- Oil marketing companies could see margin volatility

- Energy producers may benefit

💱 3. Currency Pressure

- Higher oil import bills can weaken the Indian Rupee

- This may lead to foreign investor outflows in the short term

Sector-Wise Impact: Winners and Losers

🚀 Likely Beneficiaries

- Oil and gas companies

- Upstream energy players

- Commodity-linked businesses

⚠️ Under Pressure

- Aviation sector

- FMCG companies facing input cost pressure

- Auto sector due to higher fuel costs

What Should Investors Do Now?

Geopolitical events are unpredictable, but your investment strategy does not have to be.

🧠 1. Stay Diversified

Avoid overexposure to a single sector or theme

📊 2. Focus on Quality Stocks

Companies with:

- Strong balance sheets

- Pricing power

- Stable demand

tend to perform better during uncertain times

⏳ 3. Avoid Panic Decisions

Short-term volatility is common during geopolitical tensions. Long-term investors should stay disciplined

🔍 4. Track Key Indicators

- Crude oil prices

- Inflation data

- Central bank commentary

A Real-World Perspective

We have seen similar situations in the past where geopolitical tensions led to temporary spikes in oil prices and market volatility. However, markets tend to stabilize once clarity emerges.

For example, during previous Middle East tensions, oil prices surged in the short term but normalized over time as supply adjusted.

This highlights an important lesson:

Markets react quickly, but they also adapt quickly

Why This Event Is Different

What makes this situation noteworthy is the potential policy shift toward stronger economic measures, including restrictions on oil exports.

If such actions are implemented, the impact could be more prolonged compared to past events.

FAQs

1. Why did the US-Iran talks fail?

The talks failed due to disagreements on key issues, particularly around nuclear-related commitments and compliance expectations.

2. How can this impact oil prices?

Any restriction on Iran’s oil exports can reduce global supply, leading to higher crude oil prices.

3. What does this mean for Indian investors?

It may lead to higher inflation, market volatility, and sector-specific impacts, especially in oil-sensitive industries.

4. Should investors be worried?

Short-term volatility is expected, but long-term investors should stay focused on fundamentals and avoid panic selling.

5. Which sectors benefit from rising oil prices?

Energy and oil-producing companies generally benefit, while fuel-dependent sectors may face pressure.

Conclusion

The collapse of the US-Iran talks is a reminder of how quickly global events can influence financial markets. While the immediate reaction may be volatility, the long-term impact will depend on how the situation evolves.

For Indian investors, the key is to stay informed, remain disciplined, and focus on quality investments.

At Swastika Investmart, we provide research-backed insights, advanced tools, and investor education to help you navigate such uncertain environments with confidence.

RBI’s New NBFC Rules Explained: Who Falls in the Upper Layer and Why It Matters

Key Takeaways

- RBI has simplified NBFC classification based on size and risk

- NBFCs with ₹1 lakh crore+ assets fall under the Upper Layer

- These entities will face stricter regulations and possible listing requirements

- The move aims to reduce systemic risk and improve transparency

- It can impact investors, markets, and large financial groups

Introduction

India’s financial ecosystem has evolved rapidly over the past decade, with Non-Banking Financial Companies (NBFCs) playing a critical role in credit growth. However, with size comes risk. To address this, the Reserve Bank of India has introduced a more streamlined framework to identify and regulate large NBFCs.

The new classification, especially the Upper Layer NBFCs, is a significant step toward strengthening financial stability. But what exactly does this mean, and why should investors care?

Understanding NBFC Layers: What Has Changed?

Earlier, RBI used a mix of factors like asset size, interconnectedness, and complexity to classify NBFCs. While comprehensive, this approach often lacked clarity.

The New Approach

Now, RBI has simplified the framework:

- Asset size becomes the primary criterion

- Any NBFC with ₹1 lakh crore or more in assets is categorized under the Upper Layer

This makes the system more transparent and predictable for both companies and investors.

What is an Upper Layer NBFC?

Upper Layer NBFCs are essentially systemically important financial institutions. Their size and interconnected nature mean that any disruption in their operations can impact the broader financial system.

Key Characteristics:

- Large balance sheets (₹1 lakh crore+ assets)

- High market influence

- Strong linkages with banks, markets, and borrowers

Examples (Contextual):

Large housing finance companies, infrastructure financiers, and diversified NBFC groups often fall into this category.

Stricter Rules for Upper Layer NBFCs

RBI’s objective is simple: bigger the institution, tighter the regulation.

Key Regulatory Changes:

1. Enhanced Compliance Requirements

- Tighter governance norms

- Stronger risk management frameworks

2. Mandatory Listing (in some cases)

- Upper Layer NBFCs may be required to list on stock exchanges

- This increases transparency and public accountability

3. Bank-Like Regulations

- Closer alignment with banking regulations

- Increased scrutiny on capital adequacy and asset quality

Why RBI Is Tightening the Rules

NBFCs are often referred to as “shadow banks” because they perform bank-like functions without being full-fledged banks.

The Risk Factor:

- Large NBFCs are deeply interconnected

- A failure can trigger system-wide stress

We have already seen examples in the past where NBFC stress impacted liquidity and market sentiment.

RBI’s Strategy:

- Identify large players early

- Reduce systemic risk

- Improve transparency through listing and disclosures

Market Impact: What It Means for Investors

This regulatory shift is not just a policy change. It has real implications for markets and portfolios.

1. Increased Transparency

Listed NBFCs provide:

- Better disclosures

- Regular financial reporting

👉 This helps investors make informed decisions

2. Valuation Re-rating Potential

- Companies moving toward listing may unlock value

- Institutional participation can increase

3. Short-Term Volatility

- Stricter norms may impact profitability in the short term

- Compliance costs could rise

4. Sector Consolidation

- Smaller NBFCs may struggle to scale

- Larger players could gain market share

The Tata Sons Case: A Real-World Complexity

One of the most talked-about cases is Tata Sons.

- Massive asset size puts it within the Upper Layer threshold

- However, it had surrendered its NBFC license earlier

The Dilemma:

- Should it still be regulated as an NBFC?

- If yes, will it be forced to list?

This case highlights that while the rule is simple, real-world application can be complex.

How Should Investors Approach NBFC Stocks Now?

With regulatory tightening, investors need a more selective approach.

Key Factors to Track:

- Asset quality (NPAs)

- Capital adequacy

- Governance standards

- Growth vs compliance balance

Practical Strategy:

- Prefer well-governed, large NBFCs

- Avoid over-leveraged or opaque balance sheets

- Diversify across financial sectors

Why This Move Matters for India’s Financial System

This is not just about NBFCs. It is about financial stability.

Long-Term Benefits:

- Reduced systemic risk

- Improved investor confidence

- Stronger credit ecosystem

Bigger Picture:

India’s financial markets are maturing, and such regulations bring them closer to global standards.

FAQs

1. What is an Upper Layer NBFC?

An NBFC with assets of ₹1 lakh crore or more, considered systemically important and subject to stricter regulations.

2. Why is RBI focusing on large NBFCs?

Because their failure can impact the entire financial system due to their size and interconnectedness.

3. Will all Upper Layer NBFCs be listed?

Not all, but RBI may require certain large NBFCs to list to improve transparency.

4. How does this impact investors?

It improves transparency but may also lead to short-term volatility due to stricter compliance.

5. Is this good for the market?

Yes, in the long run. It strengthens the financial system and builds investor trust.

Conclusion

RBI’s new NBFC framework marks a decisive shift toward simplification and stronger oversight. By clearly identifying large and systemically important players, the regulator aims to reduce risks before they become crises.

For investors, this creates a more transparent environment but also demands a sharper focus on quality and governance.

At Swastika Investmart, we help investors navigate such regulatory changes with in-depth research, advanced tools, and expert insights. Whether you are tracking NBFC stocks or building a diversified portfolio, staying informed is key.

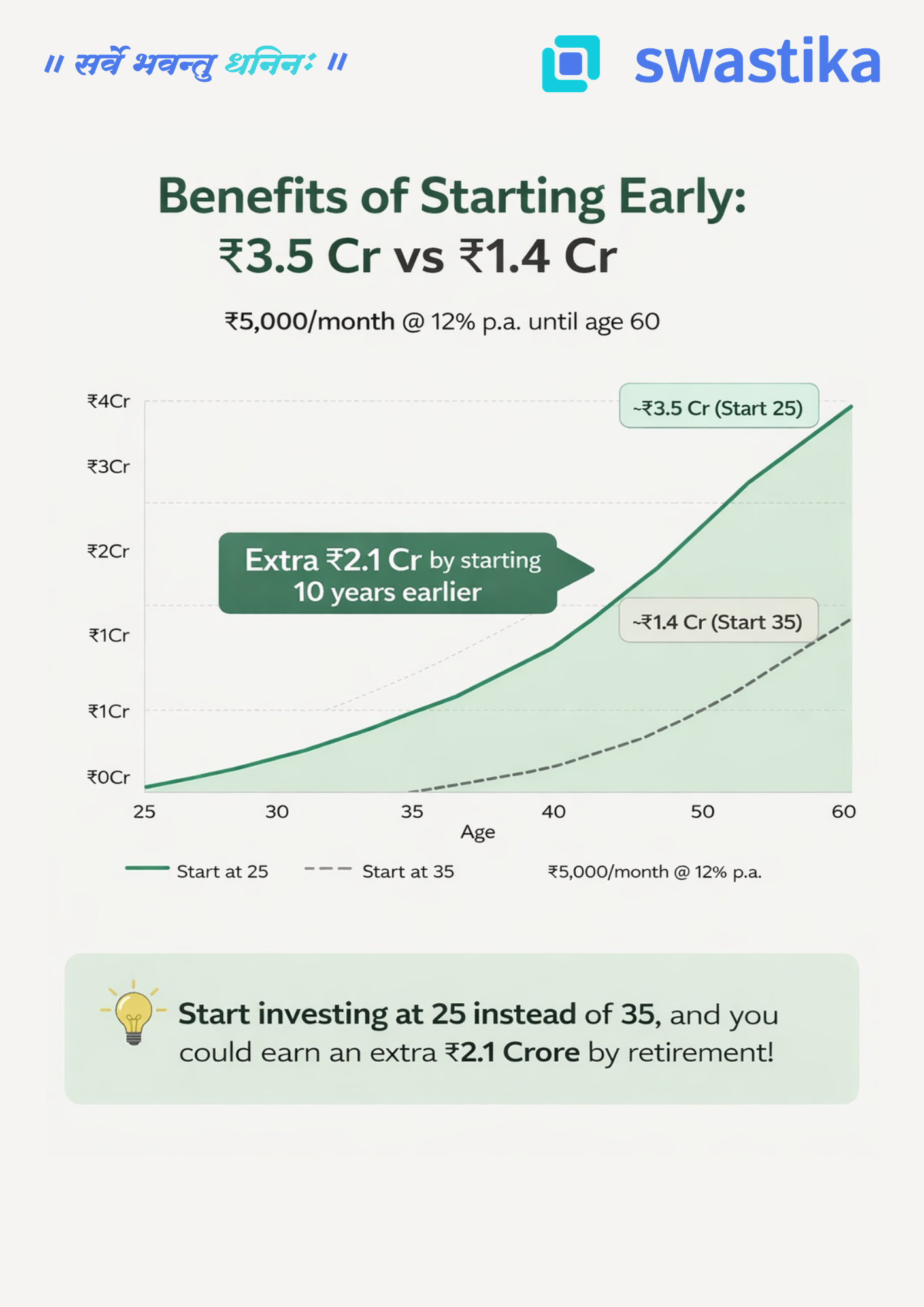

The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

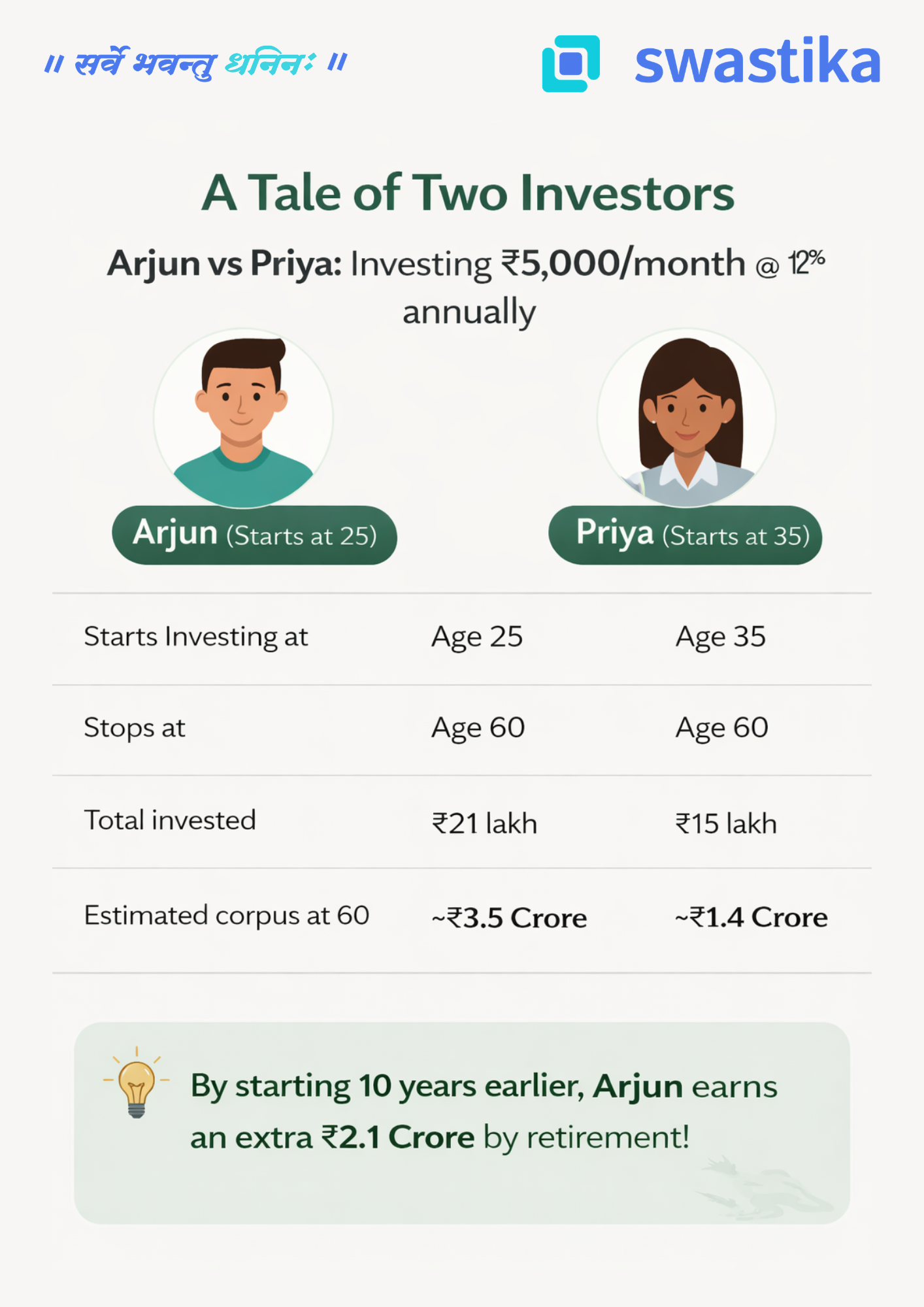

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

HRA, LTA, and Standard Deduction – Are You Claiming All Your Benefits?

Key Takeaways

- Many salaried individuals miss out on tax benefits due to lack of awareness

- HRA, LTA, and standard deduction can significantly reduce taxable income

- Choosing between old and new tax regime is crucial

- Proper documentation and planning can maximize savings

Are You Leaving Money on the Table?

Every year, millions of salaried employees in India file their income tax returns without fully utilizing available deductions.

If your salary structure includes House Rent Allowance, Leave Travel Allowance, and standard deduction, you could be saving a significant amount of tax. Yet, many people either misunderstand these benefits or fail to claim them properly.

Understanding how these components work can make a real difference in your take-home income.

Understanding HRA: More Than Just Rent

House Rent Allowance is one of the most commonly used tax-saving components for salaried individuals.

Who can claim HRA?

- Salaried employees receiving HRA as part of salary

- Individuals living in rented accommodation

How is HRA exemption calculated?

HRA exemption is the lowest of the following:

- Actual HRA received

- 50% of salary for metro cities or 40% for non-metros

- Rent paid minus 10% of salary

Real-life example

Suppose you earn ₹10 lakh annually and pay ₹25,000 monthly rent in Mumbai.

- Annual rent: ₹3 lakh

- 10% of salary: ₹1 lakh

- Eligible exemption: ₹2 lakh

This amount reduces your taxable income significantly.

Common mistake

Many taxpayers either do not submit rent receipts or assume full HRA is exempt. This leads to higher tax liability.

LTA: Travel Smart, Save Tax

Leave Travel Allowance allows you to claim tax exemption on travel expenses within India.

Key points to remember

- Covers only travel costs, not hotel or food

- Valid for two journeys in a block of four years

- Only domestic travel is allowed

Example

If you travel with your family from Delhi to Goa and spend ₹40,000 on flight tickets, this amount can be claimed under LTA.

Important tip

If you do not use LTA within the block period, the benefit lapses. Planning your travel can help you maximize this exemption.

Standard Deduction: The Simplest Tax Benefit

Standard deduction is the easiest and most straightforward tax benefit available.

Current benefit

- ₹50,000 deduction available for salaried individuals and pensioners

No bills or proofs are required. It is automatically deducted from your salary income.

Why it matters

Even though it looks small, it directly reduces taxable income and applies to almost every salaried taxpayer.

Old vs New Tax Regime: The Big Decision

One of the most critical decisions today is choosing between the old and new tax regimes.

Old Tax Regime

- Allows HRA, LTA, and other deductions

- Suitable for individuals with multiple tax-saving components

New Tax Regime

- Lower tax rates

- Limited deductions available

- Standard deduction is still applicable

What should you choose?

If your salary includes HRA and you actively claim deductions, the old regime may be more beneficial.

However, if you prefer simplicity and fewer compliances, the new regime might work better.

Impact on Indian Investors

Tax savings directly influence disposable income.

Higher savings can be redirected into:

- Equity investments

- Mutual funds

- Retirement planning

For example, saving ₹50,000 annually in taxes and investing it in equities over 10 years can create substantial wealth.

This is why tax planning is not just about saving money, but also about building long-term financial security.

Regulatory Perspective

Tax benefits like HRA, LTA, and standard deduction are governed under the Income Tax Act.

Authorities like Income Tax Department of India ensure compliance and transparency.

Taxpayers are required to maintain proper documentation and file accurate returns to avoid penalties.

Practical Tips to Maximize Benefits

1. Maintain Proper Documentation

Keep rent receipts, travel tickets, and salary slips ready.

2. Plan Travel in Advance

Use LTA strategically within block periods.

3. Review Salary Structure

Understand how your salary components are structured.

4. Choose the Right Tax Regime

Compare both regimes before filing returns.

How Swastika Investmart Can Help

Tax planning is the first step toward smart investing.

Swastika Investmart helps investors make the most of their savings through:

- SEBI-registered credibility ensuring trust

- Research-backed insights for investment planning

- Tech-enabled platforms for easy investing

- Dedicated customer support

- Strong focus on investor education

Instead of letting tax savings sit idle, you can channel them into wealth creation opportunities.

FAQs

1. Can I claim both HRA and standard deduction?

Yes, both can be claimed together under applicable conditions.

2. Is LTA available every year?

No, it is available for two journeys in a block of four years.

3. Can I claim HRA if I live in my own house?

No, HRA is only applicable if you live in rented accommodation.

4. Which tax regime is better for salaried individuals?

It depends on your deductions. The old regime is better if you claim multiple exemptions.

5. Do I need proof for standard deduction?

No, standard deduction does not require any documentation.

Conclusion

HRA, LTA, and standard deduction are powerful tools that can significantly reduce your tax burden. Yet, many individuals fail to use them effectively.

A little awareness and planning can help you retain more of your hard-earned money and put it to better use.

If you want to turn your tax savings into long-term wealth with expert guidance and smart tools, you can get started here:

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App